THE KEY TAKEAWAYS…

- San Diego’s accommodation sector is performing well as summer draws to a close.

- Hotels have been slow to rehire workers, but recent metrics suggest that a strong spate of hiring is in the cards.

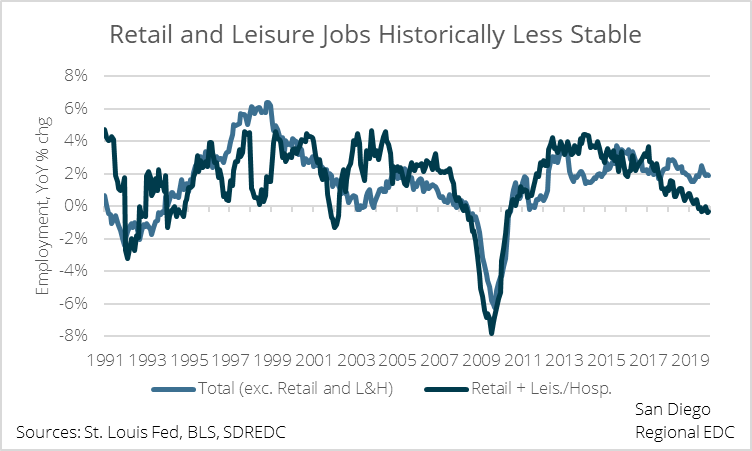

- The recovery has been uneven, but a number of industries have recouped most of the jobs lost to COVID-19.

- A number of industries still have a long way to go, and many may never recover all of the jobs lost from COVID as businesses shift their business models.

SAN DIEGO TOURISM ON THE UPSWING

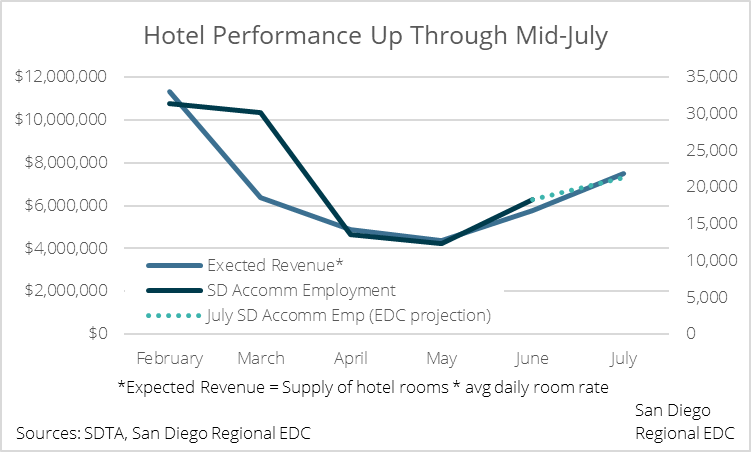

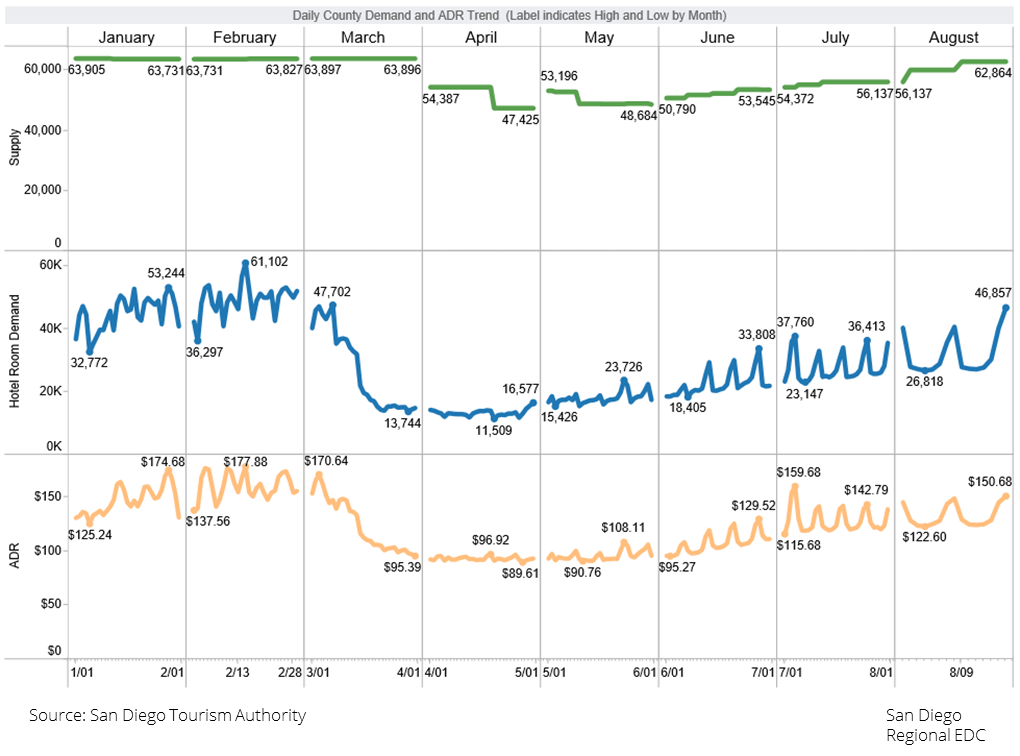

San Diego’s accommodation sector is holding its own despite another wave of COVID-related closures amid a spike in cases. Hotels in particular are closing out the summer on a high note, with the supply of rooms within striking distance of pre-COVID levels as of mid-August. The average daily rate (ADR) for rooms is climbing back somewhat more slowly but, at about $150 per night, is up some 67.4% from COVID lows in early May.

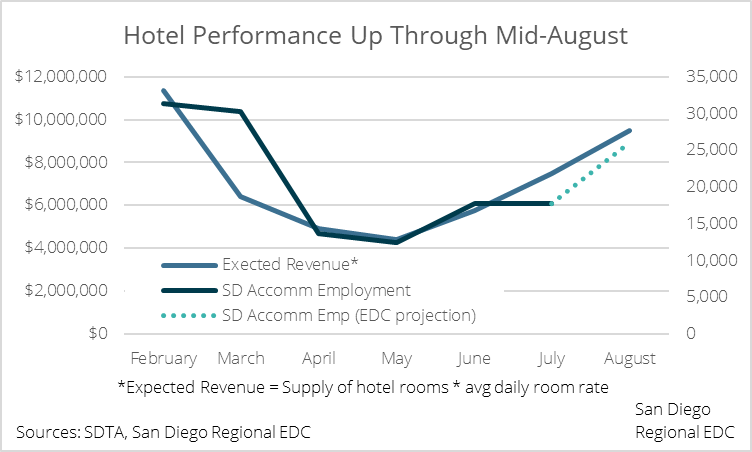

It took about a month, but as the COVID downturn intensified, accommodation employment tracked changes in room supply and average daily rates nearly one-for-one. That relationship would have suggested that accommodation employment should have grown by about 3,500 positions in July. Instead, employers only added back just 100 jobs, signaling caution on the part of hotels as the economy slowly climbs out of the crater left by the COVID-19 outbreak.

The caution within the industry makes sense. Laying off workers is painful for employers and employees alike, which is a likely reason why hotel employment didn’t falter until April and May, even though the impacts of COVID were felt as early as March. Similarly, instead of bringing workers back on just to have to let them go again in the event of another flare-up of the virus accompanied by additional closures, hotel managers may be taking a wait-and-see approach to rehiring. Nonetheless, recent industry performance suggests that hotels should be bringing about 8,000 to 8,500 workers back on to accommodate the increase in room supply and rates over the past couple of months once they feel it’s safe to do so.

As of the July employment report, accommodation employment rested at 17,800, up 43.4% from May’s low of 12,400 but still 43.3% below its pre-COVID peak of 31,400 in February. Given that expected hotel revenues—measured by the room supply multiplied by average daily rates—are just 16.5% below pre-COVID levels, employment should quickly follow. An increase of 8,000-plus employees would bring hotel employment more in line with expected foot traffic at hotels and would follow the trend seen so far during the downturn.

SAN DIEGO FACES AN UNEVEN RECOVERY

To say that the COVID downturn and subsequent recovery have been uneven across industries would be an understatement. The hotel industry’s improvement is encouraging, and a number of industries are at or near their pre-COVID employment levels, including: Heavy and civil engineering construction; building equipment contractors; computer and electronic product manufacturing; aerospace manufacturing; grocers; securities and commodities investment; and scientific research and development services.

However, total nonfarm employment in San Diego is still down 10.5% from February due in large part to slower rehiring in industries like restaurants and bars; personal services, such as dry cleaners and other laundry services as people work from home; and local government education, likely reflecting school jobs aside from teachers—like administrators, janitors, etc.—as the county waits to resume in-person teaching.

Unfortunately, many of these jobs will be slow to come back due to their face-to-face nature. What’s worse, many of those positions may not return at all. Even with the advent of a safe and effective vaccine, many businesses have changed their fundamental business models and have adopted new operational norms—like Twitter, who made working remote a permanent option for employees. As a result, the same positions required for those companies before the COVID outbreak may no longer be necessary to operate in the post-COVID world.

The impact of COVID has not only affected the lowest-paid among us in San Diego, but it has hurt communities of color the worst. Now, more than ever, targeted and effective solutions are needed to help these communities not just recover but thrive in the future. Reskilling and training of the workforce and offering equal access to capital for minority-owned businesses are not just ethical and moral necessities—they are economic ones, too. Because, we all do better when everyone is doing better; and a more resilient San Diego economy will help us all in the long-run.

Regardless of how this all plays out, EDC is here to help. You can use the button below to request our assistance with finding information, applying to relief programs, and more.

You also might like: