In April 2026, San Diego Regional EDC released its annual Inclusive Growth Progress Report, using the most up to date and available data (2024). With new progress and bold objectives set around increasing the number of quality jobs, skilled talent, and thriving households critical to the region’s competitiveness, the report measures San Diego’s growth and future outlook, and spotlights the greatest threats to prosperity.

San Diego’s economy is competitive and growing—with a GRP in 2024 that reached nearly $267 billion, 2.1% higher than in 2023, making it one of the largest county economies in the United States. This value reflects production across San Diego’s key industries including defense, tech, manufacturing, life sciences, and tourism. Yet this growth runs parallel to San Diego’s persistently high cost of living, wide income gap, and stratified opportunities across racial groups. To maintain the region’s competitiveness, the benefits of growth must be felt by more San Diego households.

Smart economic development requires sustained and intentional attention to both the region’s immediate economic growth and inclusion. To guide San Diego’s economic development priorities, EDC alongside the Brookings Institution, established an Inclusive Growth Framework. Launched in 2018 and updated annually, this initiative set ambitious goals tailored to San Diego’s unique economy and communities to achieve by 2030:

Key takeaways

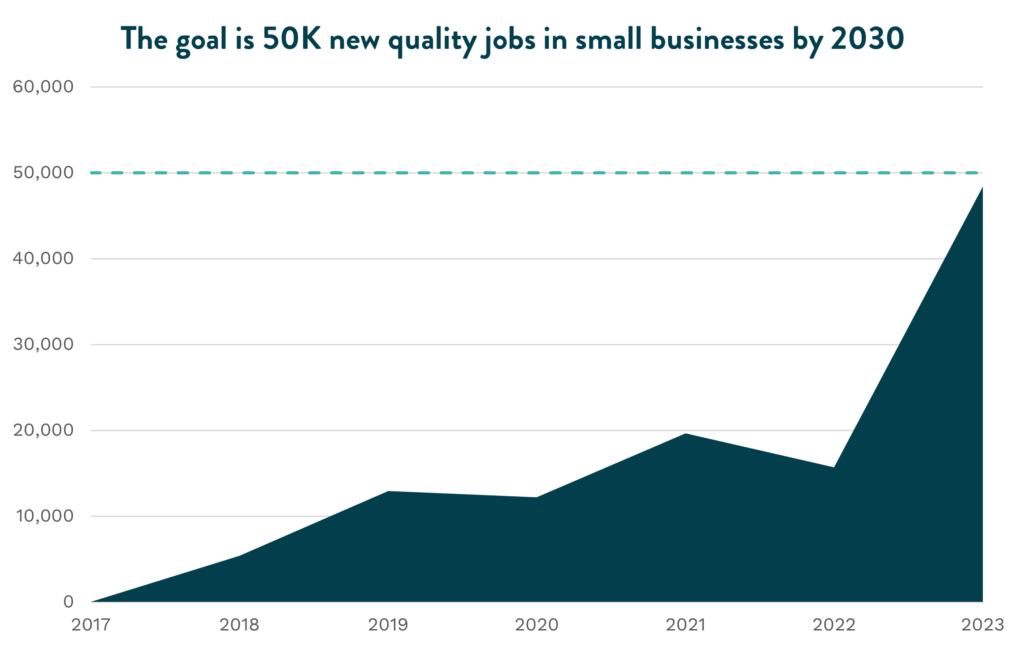

With more quality jobs in small businesses, San Diego is 87% of the way to meeting the 2030 goal. With sustained growth since 2017, the region now has a total of 228,087 quality jobs in small businesses. However, the overall proportion of quality jobs across all small businesses remains low at 28%.

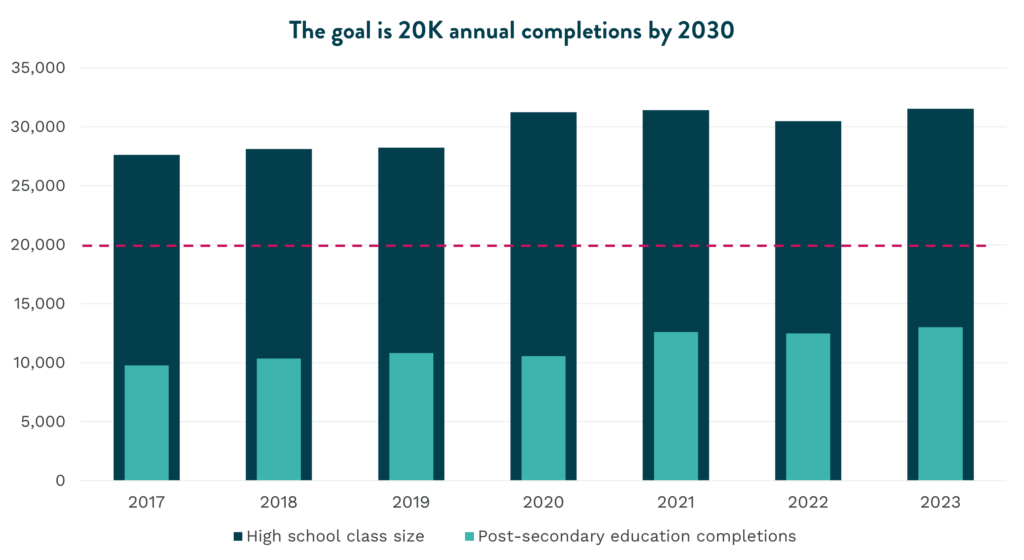

More students are succeeding, yet the region remains around 7,000 students away from the 2030 goal. Further, only 21% of those completing a post-secondary degree are Hispanic and Latinx students despite representing 49% of current K-12 students, highlighting the persistence of racial and ethnicity disparities in accessing opportunities to develop in-demand skills.

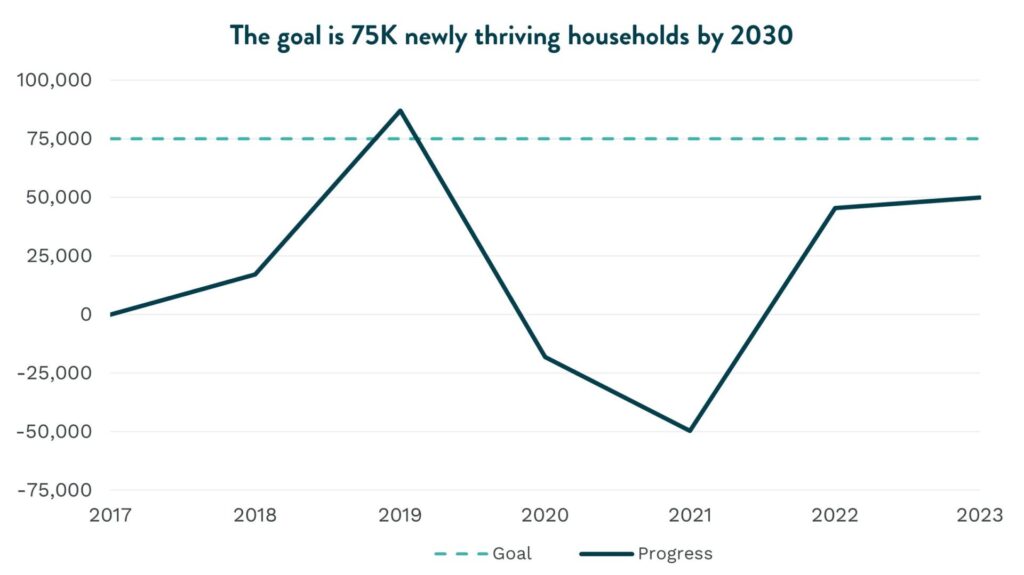

San Diego has added 38,158 newly thriving households, fewer than last year and nearly 37,000 households away from the 2030 goal. Although household income continues to grow, it is still not enough to meet the cost of living—particularly for housing—in San Diego.

The Inclusive Growth initiative is sponsored by Bank of America, County of San Diego, JPMorganChase, Lifeline Community Services, Prebys Foundation, SDG&E, and Southwest Airlines.

Petco Park remains one of San Diego’s most valuable public assets. A new analysis commissioned by the San Diego Padres and produced by San Diego Regional EDC quantifies the economic benefits generated by Petco Park based on 183 events held at the ballpark in 2024—including 85 home games, major concerts, community events and national sporting competitions—in addition to the value provided by the Gallagher Square renovation project.

In 2024, Petco Park activity resulted in about $913 million in economic impact for the San Diego region, which is equivalent to more than five Comic-Cons. These events supported nearly 15,000 jobs and generated about $1.48 billion in economic sales across San Diego County.

“The Padres take great pride as stewards of a public trust and committed civic partners, and our efforts extend well beyond the field,” said Padres CEO Erik Greupner. “Petco Park will continue to serve as a dynamic gathering place, both a ballpark and a community anchor, delivering benefits that extend far beyond the Ballpark District.”

“The San Diego Padres are more than a ballclub—they’re a cornerstone of San Diego’s identity and a powerful engine for our economy,” said EDC President and CEO Mark Cafferty. “The franchise’s impact extends far beyond Petco Park, supporting thousands of jobs and millions in economic impact, and elevating our binational identity around the globe. EDC’s report quantifies what San Diegans have long felt: the Padres inspire hometown pride, connection, and momentum year over year.”

The EDC analysis also revealed other economic impacts to San Diego, including:

Padres baseball remains the single largest driver of year-round economic activity at Petco Park, producing $9.3 million in economic impact per game due to the 40,000 fans that pack the ballpark every game.

Within the City of San Diego, Petco Park activity delivered more than $16.4 million to the General Fund and $10.5-12.4 million in annual hotel tax revenue.

The recent Gallagher Square renovation generated about $33.7 million in value added and supported 270 jobs.

Concerts and special events at Petco Park generated $123 million in regional economic impact across the county in 2024, which is expected to increase with the significant rise in non-baseball events each year.

The EDC assessment was commissioned by the San Diego Padres in Summer 2025. EDC currently does not endorse specific ballot measures or candidates. From time to time, we provide objective research on the economic impact of specific measures or proposals such as this to better inform the public and policymakers on a project’s potential economic impact. If you are interested in working with EDC on customizable research, contact us.

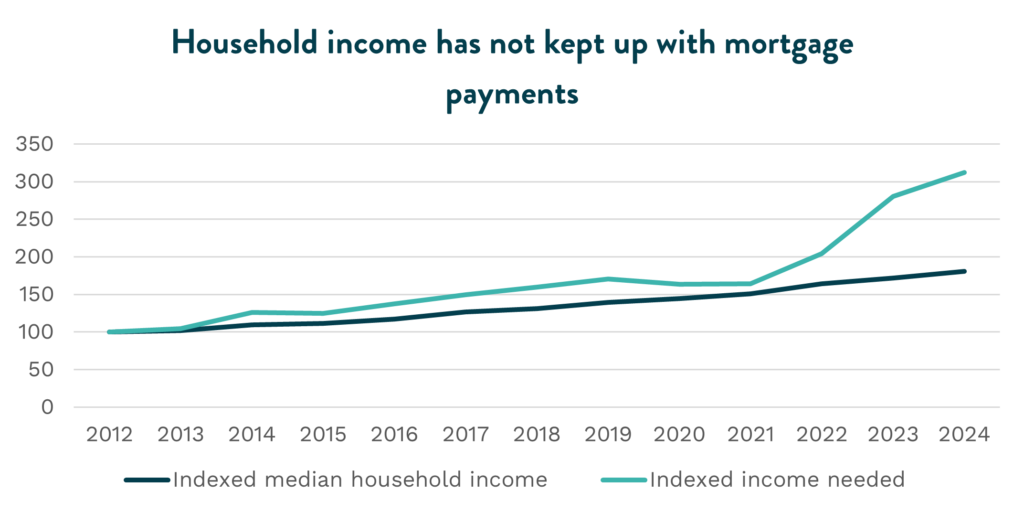

San Diego has continued to show progress in reaching our Inclusive Growth goals with 2024 median household income experiencing a 29 percent increase since 2019. Despite promising recent growth in annual earnings across the county, San Diego remains one of the most expensive metros in the U.S. By the end of 2024, households needed an income exceeding $235,000 to afford the median-priced home, a threshold that, combined with elevated interest rates, places homeownership further out of reach for most San Diegans.

On average, homeowners faced housing costs of $4,748 per month in 2024, 55.5 percent higher than 2019 costs. Because household income growth has failed to keep pace with the cost of living, the gap between local housing costs and incomes continues to widen despite home prices stabilizing.

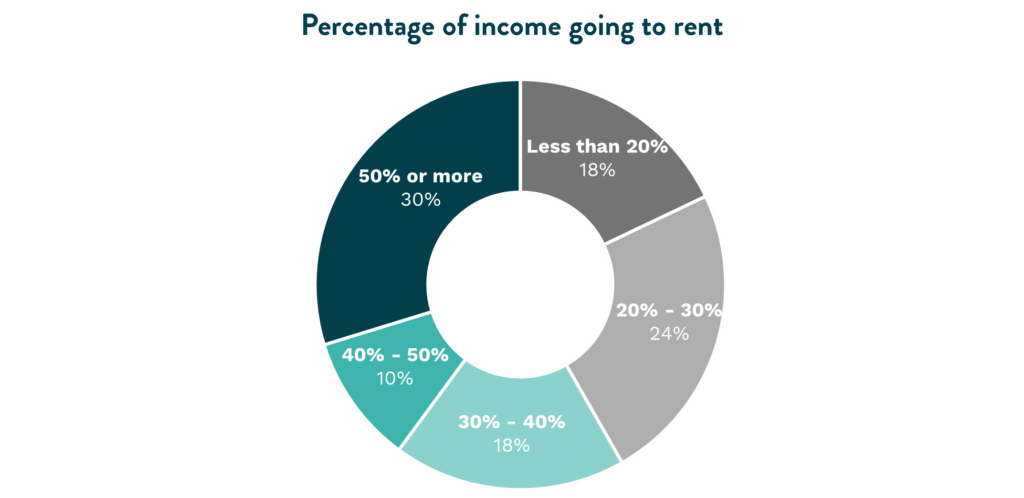

Renters face similar pressures. Average rent prices reached $4,039 in 2024, increasing by 8.3 percent over a year and 38 percent over five years. As household income struggles to catch up to increasing prices, 58 percent of renters remain cost-burdened, spending more than 30 percent of their income on rent.

Progress toward the goal

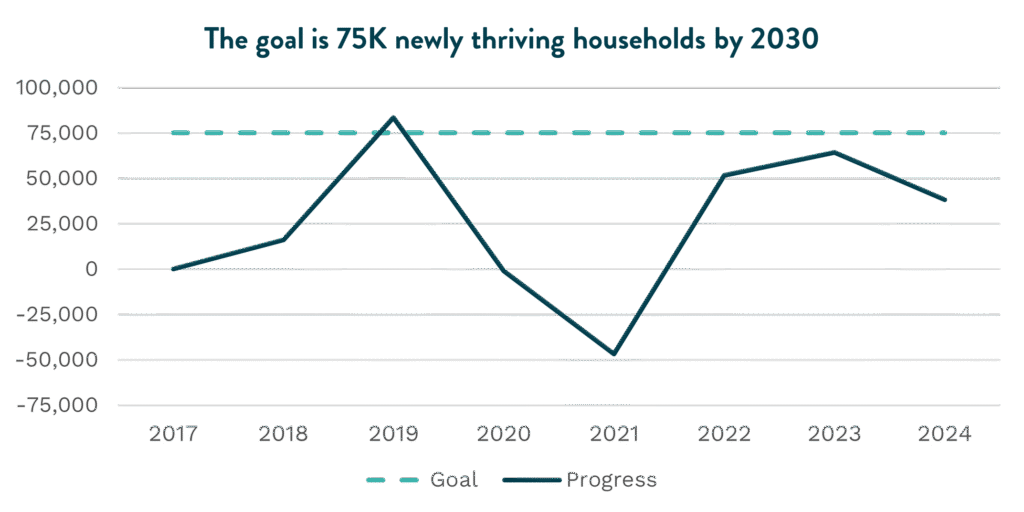

By the end of the decade, EDC estimated the region would need to add 75,000 newly thriving households. To be considered ‘thriving’ in 2024, a renter-occupied household needs at least $84,816 in household income per year, while a homeowner-occupied household needs $139,872 per year.

As of 2024, San Diego has added 38,157 newly thriving households since tracking began—a decrease from 2023 levels. The decline reflects eroding household purchasing power amid continued price pressures on essential goods including housing, groceries, and energy.

Addressing the supply challenge

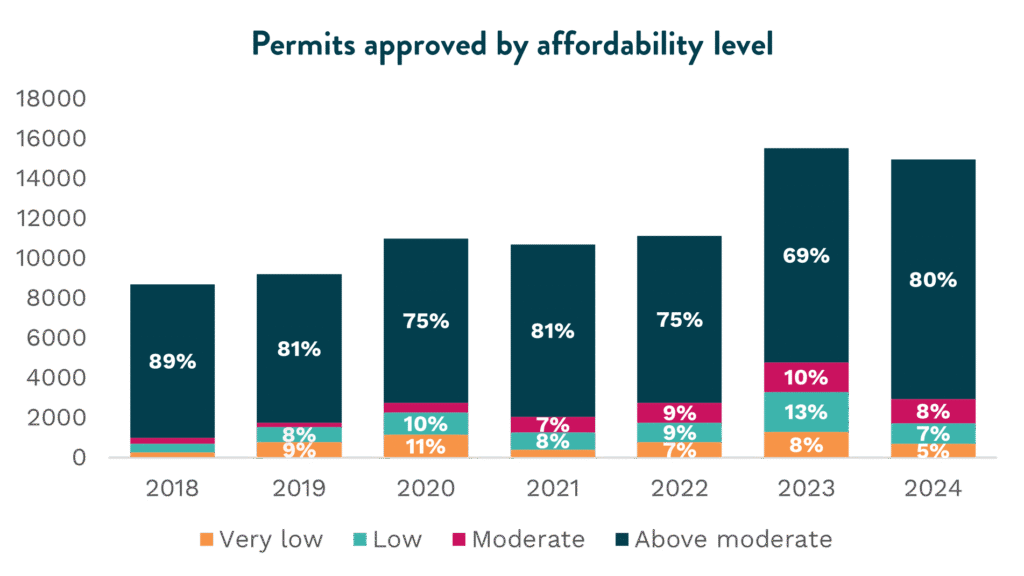

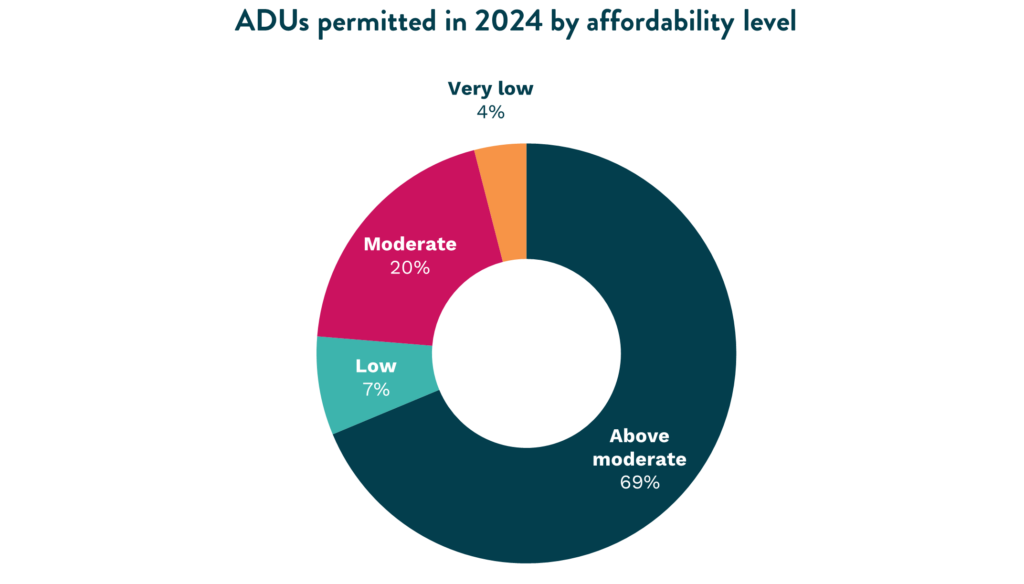

To increase housing supply, local jurisdictions have made notable progress in streamlining permitting processes. Nearly 15,000 housing permits were approved in 2024, demonstrating continued momentum despite a slight decrease from 2023. However, the number of permits for moderate income housing dropped by 18.8 percent, highlighting the persistent challenge of the “missing middle” and insufficient affordable housing production. Furthermore, permits for low and very low income households dropped 47.4 percent compared to 2023.

Accessory Dwelling Units (ADUs) represented nearly 27 percent of all permits approved in 2024—up from 22 percent in 2023—and 66 percent of all permits approved at moderate level pricing. However, those priced above moderate continue to make up most of ADU permits. While ADUs offer an opportunity to increase housing stock in existing single-family home lots, they’re unlikely to solve the region’s housing crises alone.

Developers cite several obstacles hampering housing production. The multifamily development market has become oversaturated, reducing incentives for new entrants. Current policies favor small units that do little to address the scale of San Diego’s housing needs. Rising construction costs, coupled with high insurance premiums and litigation risks, have the power to prevent projects from ever breaking ground.

At a broader level, California continues to experience a decline in construction employment, with a 1.9 percent annual decrease in 2024. This could be a potential contributing factor to slowed construction in coming years. This is especially relevant in states like California where the construction workforce is particularly reliant on immigrant workers. In fact, 40 percent of the construction workforce is comprised of foreign-born labor, potentially affecting construction-related labor under the current immigration enforcement landscape.

Extended timelines from permitting to groundbreaking further diminish project viability. Addressing these barriers will require better incentives for risk-taking and access to more flexible financing options.

Creative solutions for persistent challenges

Recent announcements signal significant office space vacancies in downtown San Diego. Major real estate firms including the Irvine Co. have been divesting San Diego office towers since 2024, reflecting broader shifts in the commercial real estate market. This challenge presents an opportunity.

Converting vacant office space into housing could revitalize areas where commercial properties no longer contribute meaningfully to the local economy. However, conversion costs can be prohibitively high. In many cases, demolishing outdated office buildings to construct multifamily housing may prove more economically feasible.

Similarly, conversions of single-family home lots into multiple single-family lots could have significant impact on housing affordability. According to LISC’s single family lot size reduction analysis, allowing multiple townhomes on one single family lot could lower home prices by 42 percent. Additionally, if 1.4 percent of the City of San Diego’s current single family lots were allowed to build multiple townhomes on one single family lot, the amount of new property taxes generated would be approximately $450 million each year, just for the County of San Diego. These innovative efforts require streamlined permitting, supportive re-zoning, and infrastructure assessment from local governments.

Identifying which vacant office properties are suited for conversion—or demolition and redevelopment—should be the first step. Addressing San Diego’s supply-constrained market will require strong public-private collaboration and regional strategies to explore innovative solutions at the scale needed to meet the region’s housing demands.

In February 2026, EDC’s Thriving Households Roundtable provided an opportunity to discuss employer-led solutions to these pressing challenges and to hear about innovative initiatives from local leaders such as LISC, cREate Development, and Center for Housing Policy and Design.

In 2020, the U.S.-Mexico-Canada Agreement (USMCA) deepened nearly three decades of North American trade. Since then, Mexico has overtaken China as the U.S.’s top trading partner, with total goods trade reaching $840 billion and capital goods imports from Mexico up 43 percent. Cali Baja itself has since evolved into one of the world’s most dynamic cross-border supply chains, where more than $2.3 billion in goods cross the U.S.–Mexico border every day, fueling industries from aerospace and medical devices to electronics and clean energy.

Against a backdrop of trade volatility and a shifting policy landscape, Cali Baja’s binational integration and co-production capabilities offer a critical opportunity to localize supply chains, strengthen North American competitiveness, and drive sustained economic growth. Yet, this same volatility, growing geopolitical tensions, and rising costs threaten to fragment this interconnected ecosystem.

“San Diego and Baja California don’t just share a border—we share an innovation ecosystem. USMCA keeps that ecosystem strong by powering advanced industries and building the resilient supply chains that define North America’s future,” said Dr. Nikia Clarke, Executive Director at World Trade Center San Diego, the report’s author. “In a world of rising tariffs and fractured trade, this is our moment to double down on this regional strength—by modernizing border infrastructure, recertifying the USMCA, and prioritizing continued investment in the binational co-production model that is our key competitive advantage.”

KEY report FINDINGS

USMCA growth reduces North American reliance on China, strengthening nearshoring opportunities. Trilateral trade has increased by 31 percent and Mexico has emerged as a dependable, highly technical manufacturing partner. Under the USMCA, capital goods imported from Mexico to the U.S., such as machinery and manufacturing equipment, surged 43 percent.

Services is the fastest-growing sector in US-Mexico trade. The integrated binational partnership extends beyond goods: In 2024, U.S. services exports to Mexico reached $50.4 billion, with imports from Mexico at $45.1 billion—increases of 54 percent and 46 percent respectively under the USMCA.

Binational trade fuels jobs and economic growth in San Diego and Imperial. Nearly 97 percent of San Diego and Imperial County’s $34.5 billion in goods exports go to Mexico, supporting roughly 95,000 jobs in critical industries like aerospace, medical device, and semiconductor.

Baja California is diversifying and moving up the value chain. Beyond traditional maquiladoras and electronics, the region now exports higher-value goods across multiple industries—including medical device and transportation equipment—compared to 15 years ago, when electronics alone accounted for 70 percent of exports.

Stability under the USMCA supports small businesses. For the 97 percent of U.S. exporters that are small businesses, a stable trade framework helps them navigate global economic uncertainty—which two-thirds identify as their top concern.

“Tijuana’s exceptional talent and proximity to San Diego create an ideal environment for nearshoring software, IT, and professional services, supporting thousands of jobs on both sides of the border,” said Maritza Diaz, Founder and CEO at ITJ. “This evolution reflects a broader shift in the binational region—from traditional manufacturing to a knowledge-driven economy that fosters innovation, integration, and global competitiveness.”

“As a global leader in aerospace, we know innovation is international. In San Diego, our access to highly skilled talent right across the border has been the difference between stagnation and growth,” said David Orth, Business Unit Director, GKN Aerospace. “Working together, our teams in Mexico and San Diego have been critical to our continued development and delivery of cutting-edge systems for commercial and defense aircraft all over the world.’’

The report was underwritten by ITJ, with sponsorship by the County of San Diego, and research support from 10 regional partners, including SANDAG, Tijuana EDC, UC San Diego, and more, and was unveiled at the 2025 Cali Baja Business Summit to an audience of 200+ binational business, academic, and civic leaders.

About World Trade Center San Diego World Trade Center San Diego (WTCSD) operates as an affiliate of San Diego Regional Economic Development Corporation (EDC). WTCSD works to further San Diego’s global competitiveness by building an export pipeline, attracting and retaining foreign investment, and increasing San Diego’s global profile abroad. WTCSD.org

In today’s hyperconnected, internet-first economy, cybersecurity is no longer optional. Whether in manufacturing, finance, healthcare, energy, or government, a single breach can inflict cascading operational, reputational, and financial consequences—reaching an average cost of $10.2 million in the U.S., according to IBM.

“San Diego continues to be a leading cyber region, with more than 1,300 firms, the Naval Information Warfare Systems Command (NAVWAR), and the highest growth of cyber certificate obtainment among our peer metros. As organizations driving innovation and strategic national priorities face increasingly costly cyberattacks, our collaborative region is developing new technologies, defenses, and cyber warriors to combat these systemic threats,” said Lisa Easterly, President and CEO, CCOE—commissioning organization of the report.

KEY report FINDINGS

San Diego’s cybersecurity cluster continues to expand, adding jobs, firms, and economic impact, even as the broader technology industry contracts. There are 14,875 jobs across 1,350 establishments within the cybersecurity cluster in San Diego, up 11 percent and 33 percent over the last two years, respectively. Together, this amounts to $4.3 billion regional economic impact and 29,040 jobs impacted.

The cybersecurity talent pool continues to grow but has been slowing down since 2022. Despite the increased need for cybersecurity professionals, the pace the talent pool grows every year is declining. This trend parallels a similar slowdown in advertised demand, as job postings for cybersecurity workers have declined and remain 60 percent lower than pre-pandemic levels.

San Diego continues to expand cyber skills, particularly in certificate obtainment, which outpaces all of San Diego’s peer metros. Overall degree and certificate obtainment in San Diego continues to grow, expanding 51 percent since 2019. Certificates, which are obtained both in and outside of traditional degree programs, have grown 78 percent from 2019 to 2023.

Business sentiment has softened. Survey results show that perceptions of San Diego’s business environment have declined relative to 2023, including access to talent, vendors, customers, and capital. Only research and development remained at the same level compared to 2023.

Amid broader technology industry declines and a shifting policy landscape, cybersecurity remains a key, growing driver of San Diego’s economy. The region’s cybersecurity cluster supports 29,000 local jobs, most concentrated at NAVWAR, the preeminent provider of information warfare capabilities for the U.S. Navy. In all, the economic impact of San Diego’s cyber cluster is equivalent to 26 Comic-Cons.

“San Diego’s cyber cluster remains a bright spot for our region, during a period of continued economic uncertainty. However, we must not take it for granted. We can continue to support its growth by connecting cybersecurity companies to new customers, more suppliers, and diverse talent that is necessary to thrive,” said Eduardo Velasquez, Senior Director of Research and Economic Development, San Diego Regional EDC.

“As cyber threats grow in frequency around the world, protecting integrated infrastructure and sensitive information across critical industries, from healthcare to defense to finance, is more important than ever,” said Rob Johnson, Vice President of Cybersecurity Sales, Thales.

Finding opportunities to navigate economic uncertainty, adapting curriculum to prepare talent for the rapidly-evolving cluster, and helping equip small business vendors to sustain cybersecurity compliance are all strategies that will help San Diego maintain its leadership in cybersecurity and innovation across the region and globe.

In partnership with CCOE, the report was sponsored by Thales, Deloitte, ESET, LevitZacks, and NDIA’s San Diego chapter, and unveiled November 12 at an industry event hosted at Qualcomm.

About Cyber Center of Excellence (CCOE) CCOE is a San Diego-based nonprofit that mobilizes industry, academia and government to grow the regional cyber economy and create a more secure digital community for all.

In October 2025, San Diego Regional EDC released “Catalyzing CA’s Fusion Advantage: Roadmap to Commercialization,” an interactive web report quantifying the economic impact of California’s fusion energy industry and exploring its potential to support more than 40,000 jobs and $125 billion to the state economy.

With electricity demand rising and climate targets tightening, the world is facing an impending energy crisis. These challenges, combined with grid instability and geopolitical vulnerability, have underscored the need for groundbreaking commercial technologies, as well as coordinated policy and regulatory frameworks to harness the state’s full potential.

The same process that powers the sun, fusion energy has long been considered the “holy grail” of power: A clean, safe, and virtually limitless source of baseload electricity. It offers high power density, no carbon emissions, minimal and short-lived radioactive waste, no risk of meltdown, and 24/7 reliability.

California has already begun to establish itself as a global leader in the fusion energy industry. The presence of industry titans such as General Atomics and TAE Technologies, coupled with world-leading R&D institutes like Lawrence Livermore National Laboratory (LLNL) and UC San Diego’s fusion cluster, positions the state as one of the world’s most promising regions for fusion commercialization. These institutions also host two of the nation’s most significant fusion research facilities—General Atomics’ DIII-D, the only operational fusion user facility in the country, and LLNL’s National Ignition Facility, where the first successful ignition proved that fusion energy is possible.

“With the right support, California can lead the in the commercialization of fusion energy, capturing the economic benefits that come from it while reshaping the global energy landscape,” said Eduardo Velasquez, Sr. Director of Research and Economic Development at San Diego Regional EDC, the report’s author. “EDC’s report brings into focus the regions, firms, and talent currently driving the industry, as well as the opportunities and hurdles the state faces in scaling from fusion R&D hub to a production powerhouse.”

Informed by nearly two dozen executive interviews with fusion business leaders, academia, and local governance, the report—available at fusionCA.org—dives deep into current industry strengths, future growth scenarios, and policy recommendations needed to drive industry competitiveness in California.

KEY FINDINGS

California leads the nation in fusion energy development. The state boasts 16 core fusion companies—more than one-third of all U.S.-based fusion companies—and has captured more than $2.2 billion in cumulative private and public funding since tracking began.

The fusion industry already generates significant economic impact—with even more high-growth potential. Currently, fusion energy accounts for approximately 4,700 jobs across California and generates $1.4 billion in annual economic output. The industry has the potential to grow to between $48 billion and $125 billion, depending on successful commercialization and state policy decisions.

California excels in research but faces commercialization challenges. The state’s world-class universities, national laboratories, and private investment ecosystem position California as the global leader in fusion R&D. However, barriers such as regulatory uncertainty, high land costs, grid interconnection delays, and lack of fusion-specific policy frameworks threaten California’s ability to retain companies as they transition from R&D to commercial deployment.

Maintaining fusion leadership requires strategic policy measures and state support. Success depends on recognizing fusion as ‘clean energy’ under state law, establishing clear regulatory pathways, preparing appropriate sites for establishing commercial research centers and fusion energy plants, and creating coordinated policy support. Without decisive action, California risks losing fusion companies to other states offering more favorable commercialization conditions.

“As a leader in climate resilience, California has been at the cutting edge of energy transition strategies and innovation for decades. Now, as fusion presents such clear economic opportunity, our state must build a long-term policy roadmap that prioritizes and incentivizes research, commercialization, workforce development, and investment to further position us to lead in the global energy transition,” said California Senator Catherine Blakespear, Chair of the Environmental Quality Committee.

“We’re proud to play a key role in advancing fusion energy here in San Diego while collaborating with partners such as the State of California, the City of San Diego, the Department of Energy, the University of California system, and national laboratories,” said Anantha Krishnan, senior vice president for the General Atomics Energy Group. “To realize our region and state’s full potential, California companies will need financial incentives, regulatory support, and streamlined land-zoning processes. In addition, public-private collaborations to build test facilities and train the future fusion workforce will be critical to achieving success in commercializing fusion energy.”

The report was underwritten by General Atomics, with research contributions by Boston Consulting Group and sponsorship by B3K Prosperity, LLNL, Livermore Lab Foundation, Mintz, ML Strategies, and Tokamak Energy, and unveiled at a press conference and industry reception October 9. Congressman Scott Peters, Senator Catherine Blakespear, and other leaders across the state were in attendance.

New analysis quantifies jobs, housing, other economic impacts for forthcoming Sports Arena redevelopment

A new analysis commissioned by Midway Rising and authored by San Diego Regional Economic Development Corporation (EDC) quantifies the projected economic and fiscal impacts of the Midway Rising redevelopment, which would revitalize nearly 50 acres of City-owned land in San Diego’s Midway/Sports Arena neighborhood.

With the addition of thousands of market-rate and designated affordable housing units, an entertainment district centered around a 16,000-seat facility, and a highly-amenitized urban park, EDC estimates Midway Rising will have a $285 million direct annual economic impact, equivalent to hosting another San Diego Comic-Con.

“This project is more than just a redevelopment—it’s a long-term investment in San Diego’s future,” said Mark Cafferty, President & CEO of San Diego Regional EDC. “As our region and state grapple with a dire affordability crisis, Midway Rising promises meaningful and accessible housing options, as well as a world-class tourism and entertainment hub that will add jobs. This is exactly the type of bold, private economic investment San Diego demands.”

Midway Rising’s more than $3.9 billion redevelopment will remake the nearly 60-year-old, City-owned Sports Arena facility and surrounding parking lot in the Midway neighborhood, and includes 4,250 new homes, a new 16,000-seat arena, and 130,000 square feet of retail space.

The EDC analysis also revealed other economic impacts to the City and neighborhood, including:

172% increase in housing stock in the Midway neighborhood.

The building of 2,000 deed-restricted affordable homes below 80 percent Area Median Income, which is the single-largest affordable housing project in California’s history.

The staffing of 3,100 permanent jobs paying 12 percent higher average wages relative to the site’s current retail mix.

A doubling of arena visitor spending from $160 million to $344 million annually.

$1.4 million in new tax revenues to the City and $3.9 million in new tax revenues to the County each year.

Participation in the City’s Business Cooperation Program, which reallocates the full 1 percent sales and use tax directly to the City’s General Fund.

Throughout the 10-year phased build-out, total construction activity is estimated to generate $3 billion in gross regional product and $94 million in tax revenues within the City of San Diego, while supporting the creation of 21,900 temporary construction jobs.

Selected by the City in late 2022, the Midway Rising team is made up of affordable housing developer Chelsea Investment Corporation, sports venue developer and operator Legends, market-rate housing developer Zephyr, and The Kroenke Group, a real estate investment company led by billionaire and professional sports team owner Stan Kroenke.

Midway Rising is anticipated to break ground in late 2026 pending City Council approval later this year.

The EDC assessment was commissioned by Midway Rising in Summer 2025. EDC currently does not endorse specific ballot measures or candidates. From time to time, we provide objective research on the economic impact of specific measures or proposals such as this to better inform the public and policymakers on a project’s potential economic impact. If you are interested in working with EDC on customizable research, contact us.

Report: Gaps in accessibility challenge the region’s goals

Today, San Diego Regional EDC released its Inclusive Growth Progress Report, using the most up to date and available data (2023). With new progress and bold objectives set around increasing the number of quality jobs, skilled talent, and thriving households critical to the region’s competitiveness, the report measures San Diego’s growth and future outlook, and spotlights the greatest threats to prosperity

Making the business case for inclusion, EDC releases this annual report to track progress toward the region’s 2030 goals: 50,000 new quality jobs* in small businesses; 20,000 skilled workers per year; and 75,000 newly thriving households**.

Since its launch in 2017, the initiative has rallied public commitments from County, City, academic, and private sector leaders who are leveraging the Inclusive Growth framework to inform their priorities, tactics, and resource allocation. While much about the economy remains uncertain and inclusion is challenged at the national level, intentional and consistent efforts by a diverse set of regional stakeholders will be key to achieving these goals.

THE STORY BEHIND THE DATA

Halfway through the decade, the San Diego region continues to make progress towards its 2030 goals with increases in quality jobs, post-secondary education completions, and median household incomes in communities of color. Nevertheless, gaps in accessibility continue to challenge the region’s competitiveness.

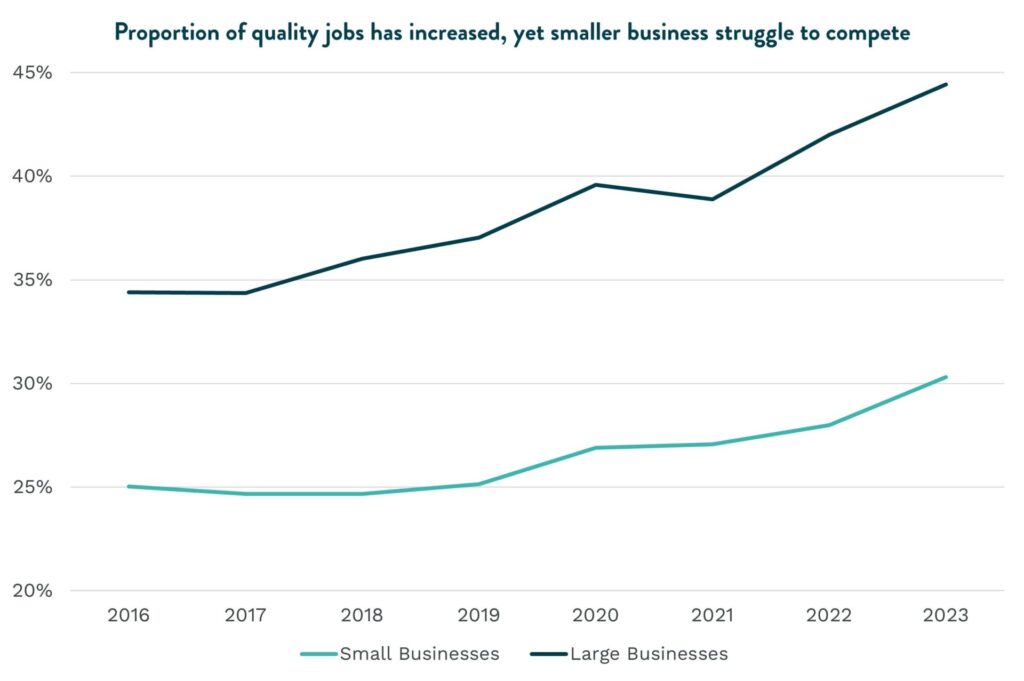

In terms of quality jobs, San Diego has made immense progress towards the 2030 goal and is even projected to exceed it. However, while quality job numbers have increased, small businesses are struggling with a stagnant pace in job growth, talent acquisition, and staff retention. These challenges further the gap between small and large businesses and threaten small businesses’ ability to compete.

With many small businesses considering leaving the region due to funding and staffing challenges, it is vital that these firms have access to new markets. San Diego anchor institutions can make an immense impact by shifting just one percent of existing procurement spend to small, local, and diverse businesses.

San Diego’s innovation economy has positioned the region as a global hub for breakthrough scientific research and life-changing technological advancements. Yet, our talent shortage poses a threat to San Diego’s competitiveness and talent goal. A key issue continues to be accessibility for low-income students who make up the workforce of tomorrow but are underrepresented in today’s workforce. While Hispanic and Latino students make up almost half of San Diego’s K-12 students, only 20 percent are currently represented in the innovation economy workforce.

Furthermore, less than 40 percent of Black and Latino students from the graduating class of 2023 were considered college-ready upon graduation, which translates into less students opting into post-secondary education. This lack of preparation, coupled with the increasing requirement of a bachelor’s degree for entry level jobs, is exacerbating the talent crisis in the innovation economy. If San Diego is going to meet workforce needs and the talent goal by 2030, greater efforts must be made to enable access and opportunity for local, young, and diverse students.

With rising housing, transportation, and grocery costs, San Diego remains one of the most expensive metros in the country. While median household incomes have seen significant growth—especially in Black and Latino households—they still struggle to keep pace with rising costs. There is also a racial disparity in San Diego’s ratio of housing wealth to population share. For example, Latino households represent 27.4 percent of the population but hold only 17 percent of the region’s housing wealth.

While not at pre-pandemic numbers yet, San Diego has added 49,916 newly thriving households as of 2023, notable progress in the face of increasing affordability pressure. In order to sustain progress, housing options must be made available at more affordable price points, and housing permit activity needs to be accelerated to meet regional goals—especially for affordable and middle-income units.

The initiative is sponsored by Bank of America, Burnham Center for Community Advancement, County of San Diego, JPMorgan Chase & Co., Prebys Foundation, SDG&E, Southwest Airlines, and TOOTRiS.

This blog post is a part of a larger series in celebration of Manufacturing Month, sharing key trends from our report on San Diego’s Manufacturing sector.

Cross-border manufacturing in San Diego has significant untapped potential. With five ports of entry, the Baja California region is one of the most accessible and lucrative for international expansion. While some companies are just beginning to explore it, many of San Diego’s most successful, innovative brands have already established a manufacturing presence in Tijuana and surrounding cities.

According to Tijuana EDC, Baja California already has 960 manufacturing facilities with plenty of room for growth. The manufacturing industry represents 65 percent of Tijuana’s GDP. Just 30 minutes to the south, manufacturing in Mexico offers cost effective products without compromising quality, backed by a steady supply of highly skilled labor.

Here are three common myths about cross-border manufacturing and how San Diego companies have been able to flourish in the binational region.

The myth: Lack of infrastructure makes it more expensive to manufacture in Mexico than advertised.

The region has made significant strides with modernizing infrastructure including upgrades to many points of entry. For example, major investments in the Otay Mesa II Port of Entry, funded primarily by the US, are set to reduce traffic congestion by up to 50 percent. This improvement will further enhance the cost efficiency of cross-border trade and manufacturing operations, making it even more attractive for San Diego companies to consider these opportunities.

Taylor Guitars is a prime example of a San Diego company benefiting from cross-border manufacturing. Its operations in Tecate are thriving due to cultural alignment and strategic advantages. A business leader at Taylor Guitars highlights the key benefits and programs it utilizes, such as the IMMEX program, which allows temporary importation of goods that are transformed or repaired and then exported.

“Manufacturing in both San Diego and Tecate gives Taylor Guitars a competitive advantage. Our Tecate operation allows us to produce quality guitars at accessible price points, reaching a broader audience, while our San Diego facility focuses on more specialized, premium instruments. Together, they enable us to deliver a diverse range of products without compromising on craftsmanship or innovation.”

– Ed Granero, VP of Product Development, Taylor Guitars

The myth: Mexico doesn’t offer high-quality manufacturing.

Many manufacturers in Tijuana work with leading global companies in high tech industries including Medical Devices, Electronics, Automotive and Aerospace. These companies require high quality and rigorous quality control measures to ensure compliance with international standards. For instance, ResMed operates a manufacturing facility in Tijuana, producing advanced medical devices like CPAP machines with stringent quality assurance protocols. Similarly, other high-tech firms like Qualcomm and Medtronic trust local partners to deliver precision-engineered products that comply with their exacting requirements.

The myth: There isn’t a strong talent pipeline present in Mexico.

The presence of high-quality manufacturing and modernized infrastructure is complemented by access to a highly capable talent pool, supported by top universities in Tijuana and advanced manufacturing capabilities in the region.

Tijuana provides a hub for a strong pool of high-skilled workers. Baja California is home to many world class universities, 37 of which are in Tijuana. Among these include top-rated schools University of Tijuana and the Tijuana Institute of Technology, which contribute to more than 3,700 annual degrees in STEM fields. Many graduates choose to remain in the region, where they can live at a lower cost and help drive the local economic growth.

Cross-border manufacturing offers San Diego companies a powerful combination of cost efficiency, advanced capabilities, and access to world class talent. By leveraging the benefits of San Diego’s proximity and relationship with Baja California, manufacturing companies not only reduce their costs but also enhance production capabilities and increase competitiveness. As infrastructure investments continue to improve cross-border logistics, and with the support of programs like IMMEX, the future looks bright for San Diego’s cross-border manufacturing landscape.

Resources to explore cross-border trade opportunities

World Trade Center San Diego and its Export Specialty Center works directly with companies—free of charge—to help them expand internationally and grow in San Diego.

Tijuana EDC provides specialized business consulting and logistics services for companies that are considering choosing contract manufacturing in Mexico to grow.

This blog post is a part of a larger series in celebration of Manufacturing Month. Click here to look at our previous deep dive on San Diego’s strong manufacturing talent pool. To read our full analytical manufacturing report click here.

This blog post is a part of a larger series in celebration of Manufacturing Month, sharing key trends from our report on San Diego’s Manufacturing sector.

San Diego’s Manufacturing sector is not just a cornerstone of the local economy; it also provides unique and well-paying career opportunities for San Diegans with great prospects for advancement. With an average wage of $103,000 per year, manufacturing jobs in San Diego pay 31 percent more than non-manufacturing jobs in the region on average. The industry supports approximately 100,000 jobs across a diverse array of industries including Craft Brewing, Life Sciences, Aerospace, and Tech as well as emerging fields like Cleantech.

Talent is a key driver for many manufacturers looking to setup or expand in the region. Companies are actively seeking local graduates, offering summer internships, and creating opportunities for individuals from historically underrepresented communities. This proactive approach to talent acquisition ensures that manufacturers in San Diego continue to thrive and innovate—and supports real San Diegans in building meaningful careers.

EDC sat down with a few local manufacturing experts to hear their experiences and insights. The goal is to showcase the diverse range of individuals and companies within the manufacturing sector and highlight the opportunities available to those interested in pursuing a career in this industry.

Employee spotlights: Real stories, real success

ASML: Working at the cutting edge of technology

Austin graduated with a degree in materials physics from UC San Diego in 2021 and holds a master’s in engineering from UC Irvine. After his stint in Orange County, he was determined to build a life in San Diego and returned to the area seeking a career in manufacturing. Although his education opened doors at top companies nationwide, Austin knew San Diego was home and was determined to carve his path here. With experience in research, he pivoted to manufacturing where he could see the direct impact of his work. Now working at local tech giant ASML on the New Product Introduction team, he integrates new products into the manufacturing process and ensures they meet customer expectations. Reflecting on his journey, Austin emphasized the importance of internships for gaining industry exposure and building professional networks. His connection to the San Diego community, formed during his undergraduate studies, has motivated him to pursue a career in the region. Austin is optimistic about the future of the semiconductor industry, noting its growth and increasing demand for chips driven by AI, and computing and electric vehicles.

TriLink BioTechnologies: Cultivating a culture of quality and inclusion

Jennifer is a dedicated member of the TriLink BioTechnologies team, part of the Maravai LifeSciences parent company, which helps other businesses develop and manufacture products vital for understanding genetic processes and developing biotechnological applications like vaccines and gene therapies. A graduate of UC San Diego, Jennifer started her career as a lab assistant in 2001, and over the years has taken on multiple roles leading to her current role as Associate Director for Quality Product Lifestyle, where she is dedicated to enhancing quality control within the company. Jennifer is passionate about mentoring and advancing female leadership in the Life Sciences industry, aiming to elevate women in executive roles. She values San Diego’s collaborative Life Sciences ecosystem, where companies share knowledge to develop life-saving treatments.

Dr. Bronner’s: Growing up in the culture of care

Blanca has navigated an inspiring career since joining Dr. Bronner’s in 2007. Joining the Vista-based company directly out of high school, she found her niche in manufacturing, driven by passion for the products she helps create. Over the years, Blanca has ascended through various roles, culminating in her current position as Director of Production. She cherishes the culture at Dr. Bronner’s, which prioritizes employee care and work-life balance, and she appreciates the company’s approach to challenges like the high cost of living in San Diego. Blanca’s experience as a woman in a traditionally male dominated industry has equipped her with resilience and determination, and inspired her advocacy for other women. Her passion for San Diego’s vibrant, inclusive culture mirrors her dedication to shaping manufacturing in the region.

Finding skilled talent for your manufacturing facilities

San Diego’s manufacturing sector is not only an economic force but it’s also a community of innovators and skilled technicians where professionals like Austin, Jennifer, and Blanca have built rewarding careers with opportunities for advancement. More than offering a job, this industry can provide fulfilment and a well-balanced and thriving lifestyle in the San Diego region.

If you’re a manufacturer looking for skilled talent like those profiled above, leverage these recruiting tools:

Develop an apprenticeship program: In partnership with Apprenti, EDC can assist companies with establishing apprenticeship programs in non-traditional fields like advanced manufacturing, information technology, cybersecurity, and more.

Connect with Verified Programs: To strengthen your company’s talent pipeline, EDC can connect employers with local post-secondary training programs that have been vetted and recognized for strong efforts to teach relevant curriculum and serve a diverse student body.

This blog post is a part of a larger series in celebration of Manufacturing Month. Click here to look at our previous deep dive on San Diego’s unique manufacturing strengths and opportunities. To read our full analytical manufacturing report click here.