In April 2026, San Diego Regional EDC released its annual Inclusive Growth Progress Report, using the most up to date and available data (2024). With new progress and bold objectives set around increasing the number of quality jobs, skilled talent, and thriving households critical to the region’s competitiveness, the report measures San Diego’s growth and future outlook, and spotlights the greatest threats to prosperity.

report at: 2025.incLUSIVesd.org

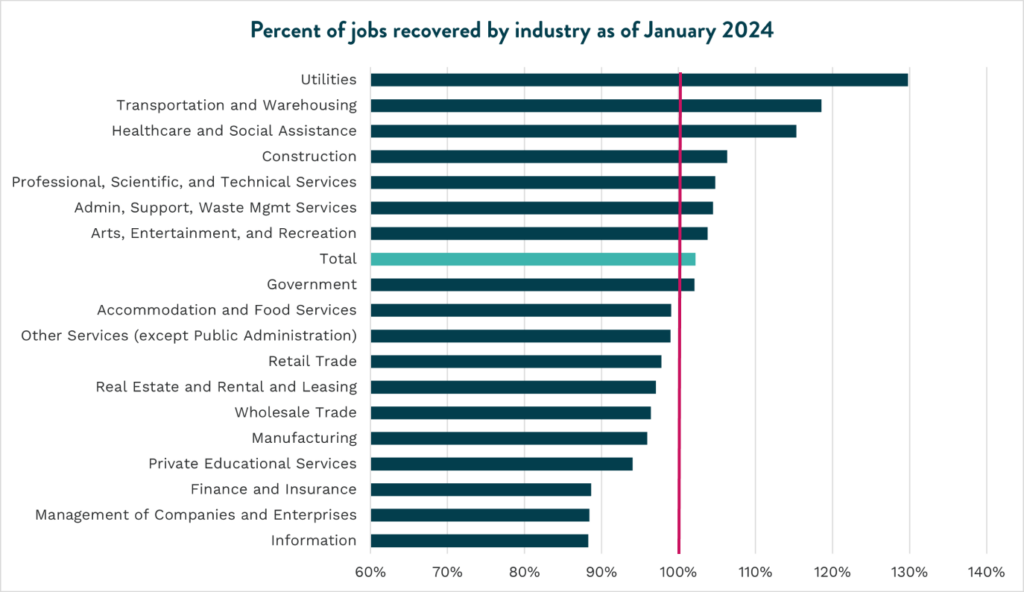

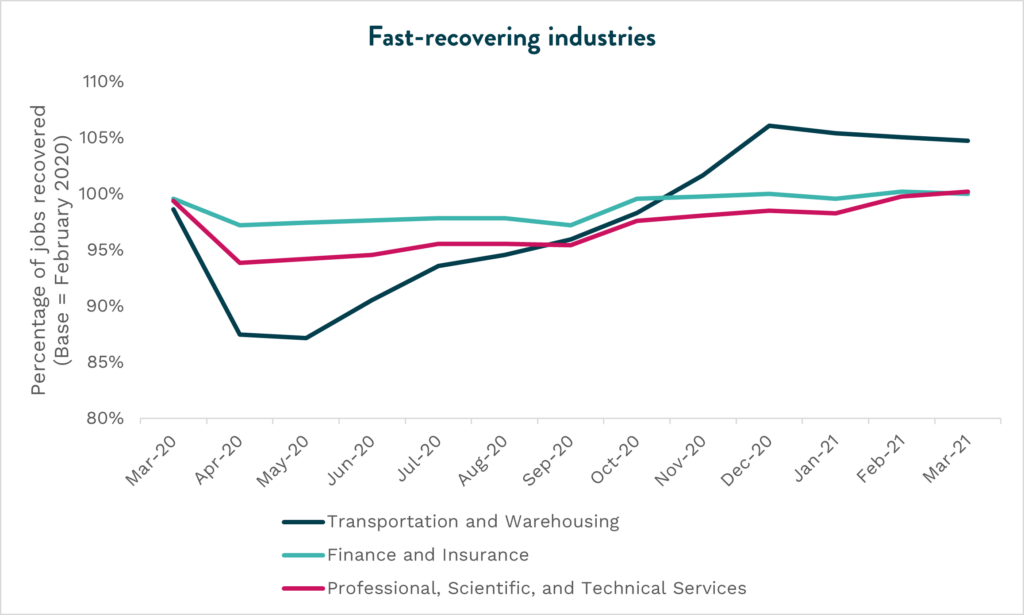

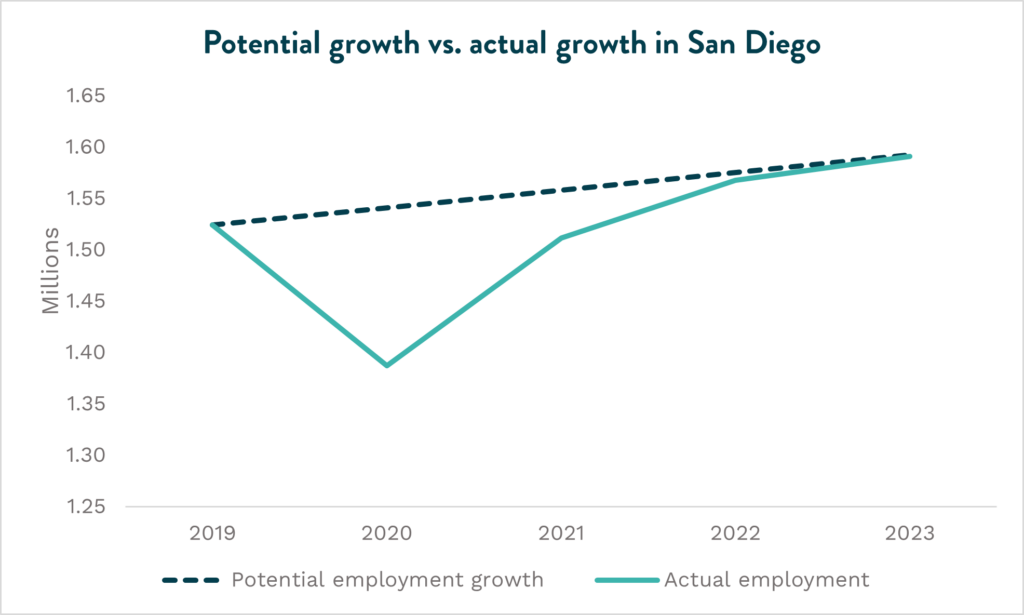

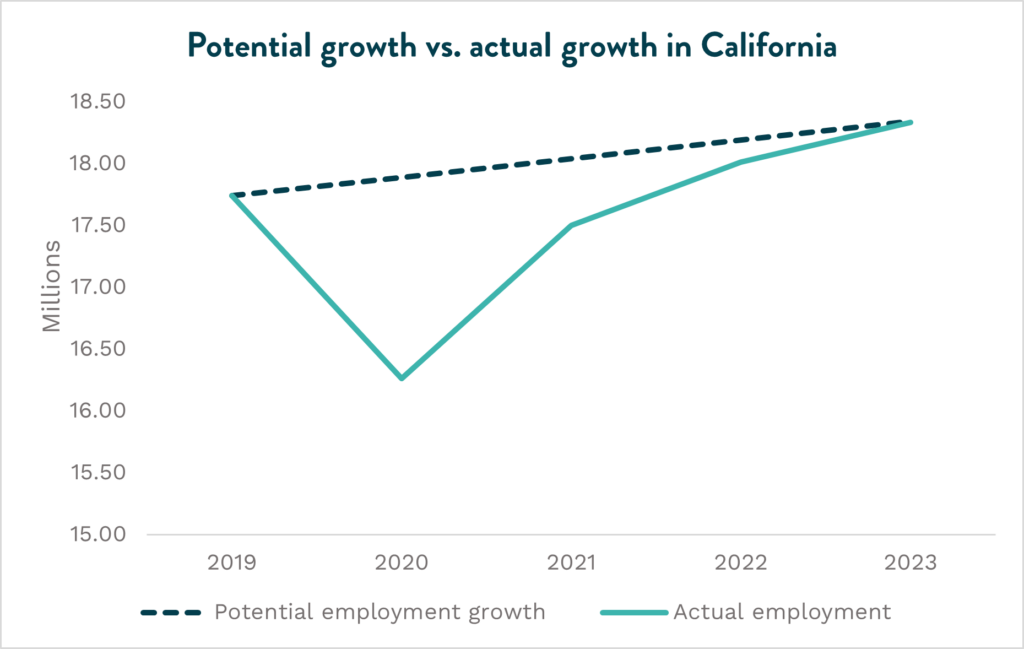

San Diego’s economy is competitive and growing—with a GRP in 2024 that reached nearly $267 billion, 2.1% higher than in 2023, making it one of the largest county economies in the United States. This value reflects production across San Diego’s key industries including defense, tech, manufacturing, life sciences, and tourism. Yet this growth runs parallel to San Diego’s persistently high cost of living, wide income gap, and stratified opportunities across racial groups. To maintain the region’s competitiveness, the benefits of growth must be felt by more San Diego households.

Smart economic development requires sustained and intentional attention to both the region’s immediate economic growth and inclusion. To guide San Diego’s economic development priorities, EDC alongside the Brookings Institution, established an Inclusive Growth Framework. Launched in 2018 and updated annually, this initiative set ambitious goals tailored to San Diego’s unique economy and communities to achieve by 2030:

Key takeaways

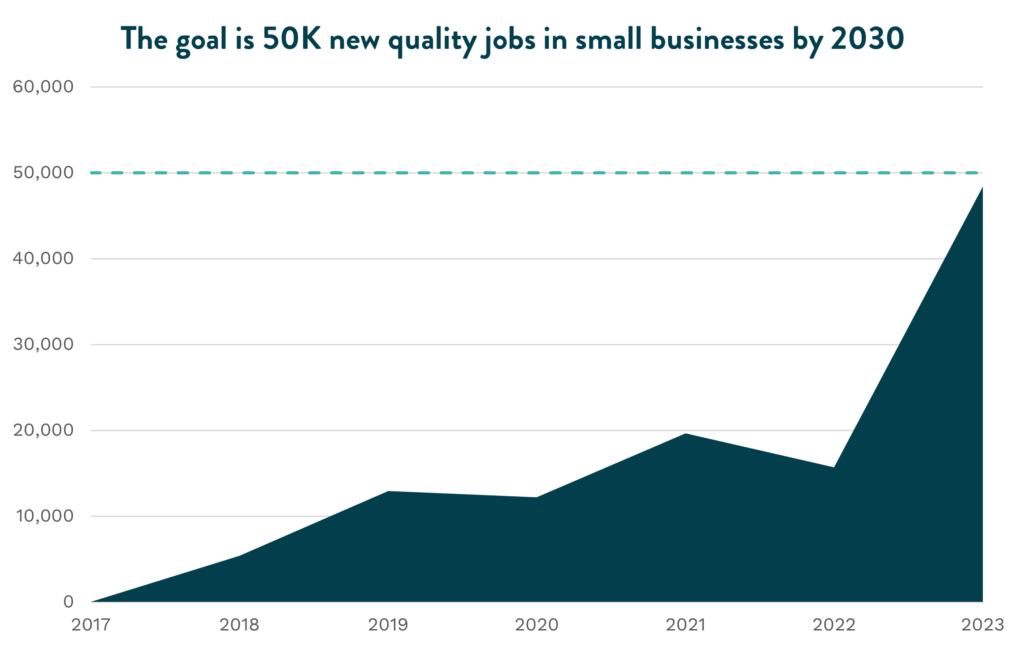

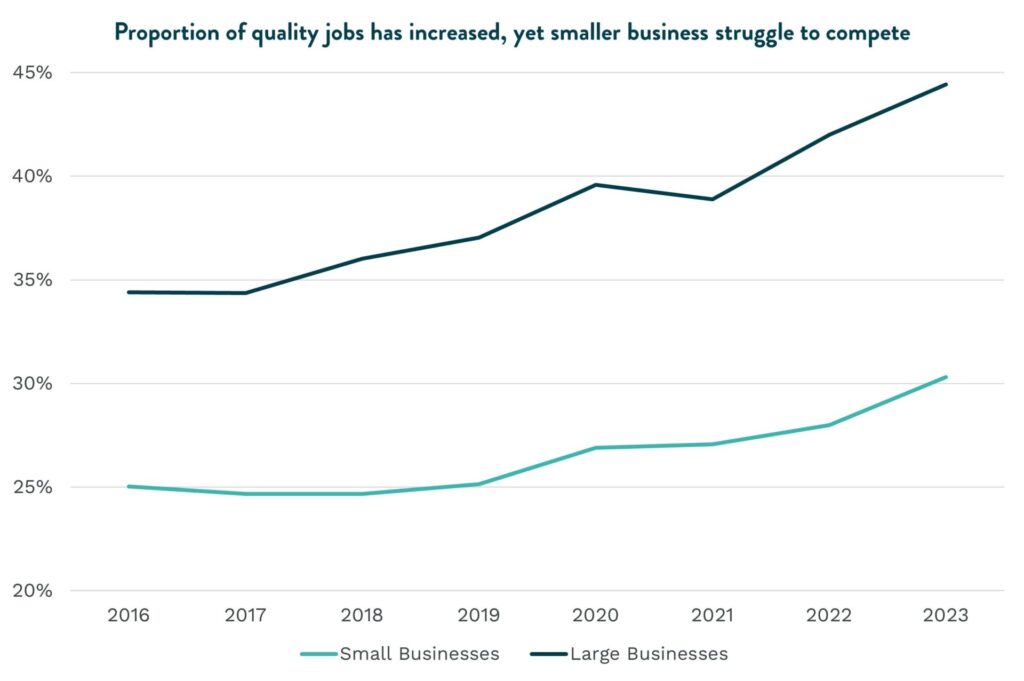

- With more quality jobs in small businesses, San Diego is 87% of the way to meeting the 2030 goal. With sustained growth since 2017, the region now has a total of 228,087 quality jobs in small businesses. However, the overall proportion of quality jobs across all small businesses remains low at 28%.

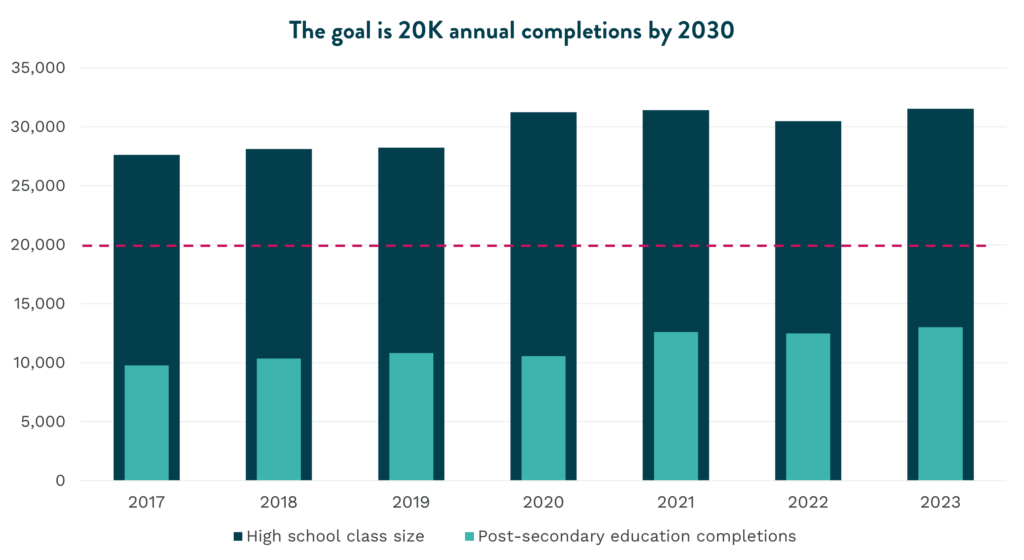

- More students are succeeding, yet the region remains around 7,000 students away from the 2030 goal. Further, only 21% of those completing a post-secondary degree are Hispanic and Latinx students despite representing 49% of current K-12 students, highlighting the persistence of racial and ethnicity disparities in accessing opportunities to develop in-demand skills.

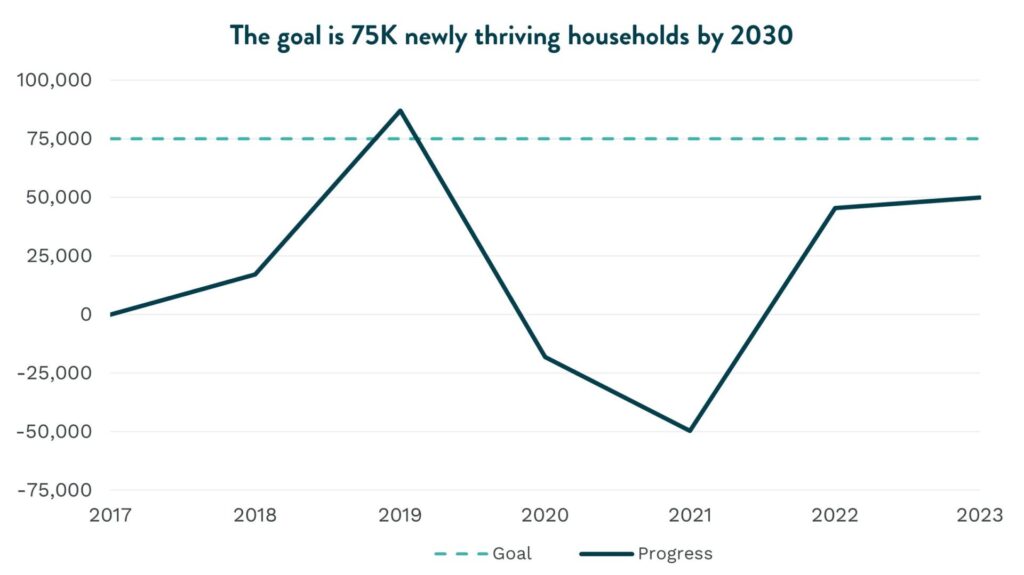

- San Diego has added 38,158 newly thriving households, fewer than last year and nearly 37,000 households away from the 2030 goal. Although household income continues to grow, it is still not enough to meet the cost of living—particularly for housing—in San Diego.

Read the full report here, and all previous updates at progress.inclusiveSD.org.

Join the movement

Learn more and get involved with EDC:

- EDC’s Inclusive Growth Report Archive

- Anchor Institutions Collaborative

- WTCSD’s MetroConnect export accelerator program

- Advancing San Diego

- Talent Data Dashboard

- San Diego Maps and Dashboards

The Inclusive Growth initiative is sponsored by Bank of America, County of San Diego, JPMorganChase, Lifeline Community Services, Prebys Foundation, SDG&E, and Southwest Airlines.