Every quarter, San Diego Regional EDC analyzes key economic indicators that are important to understanding the regional economy and the region’s standing relative to the 25 most populous metropolitan areas in the U.S.

Key findings from Q2 2022:

VENTURE CAPITAL: VC picked up speed in Q2, nearly doubling Q1 totals. The most significant increase was in San Diego’s Life Sciences sector, which jumped from $627 million to $1 billion. La Jolla-based National Resilience’s $625 million raise for biomanufacturing medicines was the largest among all sectors in Q2. Tech companies drew $593 million while Consumer companies pulled $211 million in funding.

HOUSING: San Diego housing is the second most expensive among major metros. However, the median home price remained unchanged compared to the end of last quarter, at $950,000. Q2 closed off with a total of 5,773 issued housing permits. 2021 totals reached 9,358 permits, which means 2022 permit activity is on track compared to previous years. However, issued permits might have to pass previous years totals in order to meet the housing demand in the San Diego region*.

EMPLOYMENT: Unemployment in San Diego has dropped below the national rate, at 3.2 percent. San Diego unemployment continues to approximate pre-pandemic levels (3.0 percent) and has already dropped below national pre-pandemic levels (3.4 percent). More specifically, nonfarm employment increased by 17,700 during Q2, and by 79,700 compared to a year ago. Leisure and Hospitality employment continues to increase for the fifth consecutive month, and currently represents around 10 percent of the sector in California (EDD).

*Data correction: Please note that the initially published Key Takeaways from Q2 2022 erroneously stated the number of housing permits for 2021 and 2022 YTD. The written summary has been updated with the correct values.

Every quarter San Diego Regional EDC analyzes key economic indicators that are important to understanding the regional economy and the region’s standing relative to the 25 most populous metropolitan areas in the U.S.

EDC explains San Diego’s Q1 2022 economic data:

Key Findings from Q1 2022:

VENTURE CAPITAL: Strong VC funding in Life Sciences continues despite uncertainty surrounding inflation. Although high inflation and rising interest rates have been a concern recently, investments in Life Sciences companies only fell by about $10 million to $632 million from Q4, while investments in Tech companies returned to average levels. Total investment into the region exceeded $1 billion in Q1, an increase of more than $250 million compared to the quarterly average for 2019.

COMMERCIAL REAL ESTATE: Demand for lab space has a greater impact on CRE market than remote work arrangements. As businesses embrace hybrid and remote work, there is uncertainty surrounding the impact to the commercial real estate market. Data show that businesses are not completely abandoning the office, with many adopting hybrid work schedules that will only lead to a one to two percent reduction in office space requirements nationally. In San Diego, demand from the Life Sciences industry is even stronger, resulting in a seven percent increase in asking rates for lab space from Q4. According to CBRE, 6.5 million square feet of planned conversions and construction are expected to become available in the next three years.

HOUSING: Home prices continue to soar despite fewer sales. The median home price in San Diego continues to climb, reaching $950,000 in March. This translates to an 18.8 percent increase in the median home price compared to March 2021. In fact, the year-ago increase in home prices has hovered consistently around 15 percent since August 2021, almost double the rate of inflation we have seen over the past 12 months. While rising mortgage rates have the potential to temper the housing market, the median home price continues to rise at a faster rate than the national average.

Presented by Meyers Nave, this edition of San Diego’s Data Bites covers March 2022, with data on employment and more insights about the region’s economy at this moment in time. Check out EDC’s Research Bureau for even more data and stats about San Diego.

KEY TAKEAWAYS

San Diego employers added 8,000 nonfarm payroll positions between February and March, lowering the unemployment rate to 3.4 percent from a revised 4.0 percent from one month ago.

Compared to March 2021, total nonfarm employment increased by 103,600, or 7.4 percent. 49,900 additional jobs in Leisure and Hospitality led year-ago employment gains, with Professional and Business services adding 20,600 positions.

Employment in San Diego lags pre-pandemic levels by only 14,000 jobs, with Leisure and Hospitality accounting for 9,000 missing payroll positions. However, industries in San Diego’s innovation economy are well ahead of where they were before COVID-19.

Unemployment rate drops below four percent in March 2022

The March employment report showed that San Diego establishments added 8,000 nonfarm payroll positions compared to February, with 5,000 of these jobs in Leisure and Hospitality. State and Local Government was the next-closest industry experiencing employment gains, with 2,000 additional jobs. These additions to San Diego’s economy drove the unemployment rate lower by 0.6 percentage points, from a revised 4.0 percent in February to 3.4 percent in March.

Health Care and Social Assistance lost the most jobs between February and March, dropping 1,300 payroll positions. Although Ambulatory Health Care Services accounted for 1,100 of the lost jobs, the industry employed more people in March 2022 compared to pre-pandemic levels in February 2020. These lost jobs could be the result of lower transmission and infection rates of COVID, requiring fewer employees to manage workloads.

Leisure and Hospitality continues to lead year-ago employment gains

Overall, San Diego employers added 103,600 nonfarm payroll positions from March 2021 to March 2022. Leisure and Hospitality accounted for 49,900 of these jobs, which is not surprising considering that companies in this industry cluster were the hardest hit by the pandemic. The fact that businesses engaged in Accommodation and Food Services are adding more jobs with each new jobs report is a sign that San Diego is recovering well from the troughs of the pandemic.

Furthermore, not a single one of the industry clusters that the EDD tracks (e.g. Leisure and Hospitality and Professional and Business Services) showed year-ago jobs losses, providing further evidence of the steady recovery of San Diego’s economy back to pre-pandemic levels. Professional and Business Services added 20,600 positions to San Diego’s economy, a 7.9 percent increase over last year’s levels. As part of San Diego’s innovation economy, industries such as Scientific Research and Development Services tend to be comprised of quality jobs, those that offer economic security by paying a wage that keeps up with the cost of living and providing employer-sponsored health benefits. Some sub-industries, however, did shed jobs compared to a year ago, such as Nursing and Residential Care Facilities (down 2,300 jobs) and Durable Goods manufacturing (down 2,000 jobs).

Employment in San Diego lags pre-pandemic levels by only 14,000 jobs

San Diego’s total nonfarm employment ended March 2022 at 1,501,100 jobs, which is 14,000 shy of pre-pandemic levels in February 2020. Although employment in Leisure and Hospitality is still 9,000 jobs lower than before COVID-19, this industry cluster has consistently led the pack in each monthly jobs report, meaning that pre-pandemic levels are just within reach. This is a strong indicator of the region’s economic recovery and health, as Accommodation and Food Services companies were the hardest hit by the pandemic.

Employment in other industry clusters, including those that drive San Diego’s innovation economy, has already surpassed pre-pandemic levels. Professional and Business Services has added almost 20,000 positions to the region’s economy from February 2020, with 7,300 of these jobs belonging to Scientific Research and Development Services. Jobs in these industries often have a high concentration of high paying quality jobs. The record year that San Diego experienced with respect to venture capital—especially in Tech and Life Sciences companies—should result in even more hiring by these companies throughout 2022.

However, the economic stimulus over the course of the pandemic has resulted in the highest inflation seen for quite some time, with the 12-month inflation rate reaching 8.5 percent in March. This led the Federal Reserve to hike interest rates by 25 basis points, with expectations of more to come. These expectations have translated into a decreased appetite for borrowing and investment, slowing the record pace at which San Diego is attracting venture capital dollars.

In fact, investment in Series A, seed, angel, and growth stages totaled just over $1 billion in Q1 2022, a far cry from the $2.7 billion in Q1 last year. Though the rate at which money is flowing into San Diego Tech and Life Sciences companies is slowing, the region will feel the ripple effects of the record-setting year in 2021 for some time to come. For example, the current demand for lab space in San Diego County is triple the amount of new deliveries that are expected in the next 12 months. As these Life Sciences companies move into new commercial space in the region, they will need to hire for newly created positions, many of which are high-paying quality jobs.

However, San Diego companies across all industries are engaged in a bitter competition for talent. Not only do high levels of inflation make San Diego a more expensive place to live, but a white-hot housing market has sent home prices through the roof, with the median home price reaching $950,000 in March, a 19 percent increase from one year ago. This high cost of living in San Diego is a tax that deters talent from staying in or relocating to the region. By addressing San Diego’s affordability crisis and building San Diego’s talent pipeline, employers can do their part to bolster the region’s resiliency and global competitiveness.

County, City, academic, and private sector leaders announce commitment to inclusive economic growth

Today at its Report to the Community event, San Diego Regional EDC shared progress against the 2030 inclusive growth goals outlined pre-pandemic in 2018. With new data and bold objectives set around increasing the number of skilled talent, quality jobs, and thriving households critical to the region’s competitiveness, County and City of San Diego officials as well as leaders in the private sector, education, and philanthropy offered their shared commitments to economic inclusion.

“EDC’s recent analysis underscores the significant impact of the pandemic on San Diego’s under-resourced communities and small businesses,” said Julian Parra, Business Banking Region Executive at Bank of America and EDC Board Chair. “To drive meaningful economic change, a diverse set of stakeholders must step up or the issues facing our economy—talent shortages, skills gaps, and a soaring cost of living—will further challenge San Diego’s economic competitiveness.”

The innovation economy has made San Diego more prosperous than many of its peers—leading the region out of the COVID-spurred economic recession as it has in past downturns—but remains inaccessible to the fastest-growing segment of the region’s population. At no surprise, the goalposts EDC outlined four years ago are now farther from reach in the wake of the pandemic.

With nearly 200 members, EDC represents just a small fraction of the region’s employers. It is only with and through a broader group of stakeholders that more quality jobs, skilled talent, and thriving households in San Diego is possible. As such, EDC has enlisted the endorsement of key regional partners and employers that have committed to using the Inclusive Growth framework to inform their priorities, tactics, and resource allocation.

Hear some of those commitments:

“The County shares a deep commitment to the framework outlined by EDC. In order to help regionalize these Inclusive Growth goals, the County has created the Office of Economic Prosperity and Community Development that will prioritize significant investments in our communities as well as uplift our local businesses,” saidVice Chair Nora Vargas, San Diego County Board of Supervisors. “Our inclusive work is centered on achieving an equitable economic recovery that ensures prosperity for all San Diegans.”

“Employing more than 1,200 San Diegans, we understand the criticality of large employers fostering a robust talent pipeline who can afford to live and thrive here,” said Jennie Brooks, Senior Vice President at Booz Allen Hamilton and EDC Vice Chair. “We are committed to advancing these goals by mentoring the next generation of women leaders through partnerships with local organizations like Girl Scouts San Diego; creating opportunities through our Mil/Tech Workforce Initiative to help military veterans build on their experiences and upskill into quality tech careers; and providing the flexibility that employees need in today’s dynamic work-life environment.”

The pandemic’s impact to progress: Jobs, talent, households

In its new analysis, available at progress.inclusivesd.org, EDC quantifies the COVID-19 pandemic’s devastating impact on the regional economy and reports progress toward the 2030 goals. Takeaways include:

QUALITY JOBS: While the region saw an overall increase in the number of quality jobs* since 2017, the disparity between quality jobs in small and large firms grew. The jobs losses of 2020 were principally concentrated in lower paying jobs at small businesses, especially those held by people of color. Meanwhile, larger firms added quality jobs in haste. In order to compete on talent, small businesses need new, reliable customers. San Diego’s large buyers can support quality job growth and ensure supply chain resilience by spending more with small, local businesses.

SKILLED TALENT: Since 2016, all job growth has been in positions that require some form of degree or credential acquired through post-secondary education (PSE). Looking forward, it is projected that 84 percent of new jobs created between now and 2030 will also require PSE. Hispanics represent one-third of San Diego’s total population but only 15 percent of degree holders. Further, nearly half of middle school students are Hispanic but are statistically the least prepared for the jobs of the future. To address employers’ hiring challenges long-term, the region must invest in college readiness for more San Diego students.

THRIVING HOUSEHOLDS: Rapidly rising home prices—up more than 30 percent in the last two years alone—coupled with jobs losses have resulted in almost 11,000 fewer thriving households** in 2020 than in 2017. Further, the region lost 3,200 licensed childcare facilities due to business closures amid the pandemic. Rising costs and access to childcare, transportation, and broadband—disproportionately felt by people of color—will leave businesses unable to retain or recruit talent from outside of the region.

While the innovation cluster has more than rebounded from the pandemic, the talent challenges employers face will only worsen and threaten their growth across San Diego. A concerted commitment to Inclusive Growth must be made; the region’s competitiveness depends on it.

The initiative is sponsored by Bank of America, HomeFed Corporation, San Diego Gas & Electric, Southwest Airlines, The San Diego Foundation, University of San Diego School of Business, City of San Diego, and County of San Diego.

Presented by Meyers Nave, this edition of San Diego’s Data Bites covers January and February 2022, as well as an additional update on annual benchmark revisions, with data on employment and more insights about the region’s economy at this moment in time. Check out EDC’s Research Bureau for even more data and stats about San Diego.

KEY TAKEAWAYS

San Diego’s unemployment rate dropped by 0.7 percentage points–from a revised 4.7 percent in January to 4 percent in February–with nonfarm employment increasing by 16,500 payroll positions.

Employers in the region added more than 104,000 payroll positions since February 2021–with Service Providing industries accounting for 102,600 of the added jobs–lowering the unemployment rate by 3.7 percentage points.

Annual benchmark revisions to employment data show that the region’s economy was recovering more rapidly than initially believed. Specifically, revisions to nonfarm employment for December 2021 improved the jobs count by more than 40,000 workers.

Service Providing industries lead month-ago and year-ago changes

February’s jobs report painted a positive picture for the San Diego regional economy. With respect to changes from January to February, nonfarm employment increased by 16,500, driving the unemployment rate lower to 4 percent from a revised 4.7 percent in January. Service Providing industries led the pack in employment gains, as Professional and Business Services added 6,100 jobs, Educational and Health Services added 4,800 jobs, and Leisure and Hospitality added 4,200 jobs. Trade, Transportation, and Utilities dropped 2,700 jobs, however, with employers in Retail Trade shedding 2,300 payroll positions. Manufacturing industries also had a down month, with losses of 1,000 jobs in Durable Goods production.

Service Providing industries were also the leaders in year-ago employment gains from February 2021, adding more than 104,000 jobs to the region. The slow and steady employment gains over the last year have resulted in the unemployment rate dropping by almost four percentage points from a revised 7.9 percent in February 2021 to 4 percent in February 2022. Within the Service Providing sector, Leisure and Hospitality added 52,700 positions, which is a good sign of recovery as these companies were the hardest hit during the pandemic. Employers in Professional and Business services also added 21,100 payroll positions, 9,300 of which were in Professional, Scientific, and Technical Services. These gains were not felt across all industries, however, as Durable Goods manufacturing lost 1,900 jobs from February 2021.

February employment inches closer to pre-pandemic levels

Looking at changes from February 2020 to February 2022 shows that the region is getting ever closer to pre-pandemic levels, a good sign for the recovery of San Diego’s economy. Total nonfarm employment is only about 25,000 (1.64 percent) lower than before the pandemic. Over half of these missing jobs are in Leisure and Hospitality, as the industry shows 14,000 fewer jobs in February 2022 than the same month in 2020, a gap of around 7 percent. Durable goods manufacturing is also exhibiting signs of a slower recovery with 6,200 fewer payroll positions than before the pandemic, or about 7 percent lower.

Despite some industries still playing catch-up, many have surpassed pre-pandemic employment levels. Professional and Business Services employers have added 19,300 payroll positions since February 2020, an increase of 7.4 percent. Notably, Administrative and Support and Waste Services have added 11,000 jobs (up 12.4 percent) while Professional, Scientific, and Technical Services have increased employment by 8,900 (up 6.05 percent). Speaking to San Diego’s position as a leader in Innovation and Life Sciences, companies in Scientific Research and Development Services have added 7,300 jobs since the start of the pandemic, an increase of more than 20 percent. With a hiring frenzy in innovation-related industries in full force, it is imperative for our region’s competitiveness that we continue to bolster the supply of the skilled labor that San Diego companies demand.

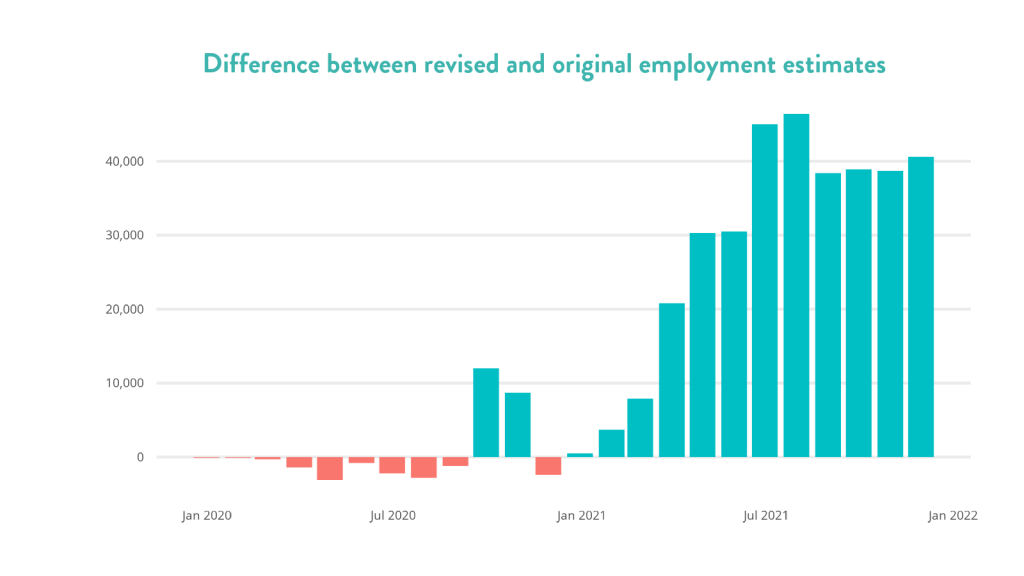

Annual revisions show employment was greater during 2021 than first believed

Every March, the California Employment Development Division works with the Bureau of Labor Statistics to revise employment data, a process called benchmarking. Depending on the year and the difficulties in gathering accurate employment data, these revisions might be significant. For reasons that should be unsurprising by now, 2021 was one such year.

What is striking about these revisions is the increasing underestimation of employment throughout 2021. Although January’s revised employment count was only about 500 greater than original estimates, the number had grown to 40,600 by December 2021. Put another way, original estimates were about 3 percent lower than the revised numbers. While this may seem like a trivial distinction, it does indicate that San Diego’s economic recovery was even stronger than originally believed. In fact, the industries that were most impacted by the pandemic reported some of largest upward revisions.

Leisure and Hospitality had 14,600 more jobs in December 2021 with the revised numbers (an upward revision of 8.7 percent), being driven by 8,500 jobs in Accommodation and Food Services (an upward revision of 5.8 percent). Revisions increased the employment count in Professional and Business Services by 12,100 (an upward revision of 4.5 percent), largely attributable to changes in Administrative and Support Services (an upward revision of 7,400, or 8.7 percent). All industries did not show an increase due to the annual revisions, however. Employment in Construction was lowered by 2,900 jobs (a downward revision of 3.4 percent) while the jobs count in Retail Trade was decreased by 2,100 jobs (a downward revision of 1.4 percent).

Welcome to the final edition in EDC’s Changing Business Landscape Series, which is published bi-monthly in the San Diego Business Journal and here on our blog. If you missed them, check out all past editions here.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. Companies in every industry are rapidly re-evaluating how they do business, changing the way they interact with customers, manage supply chains and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

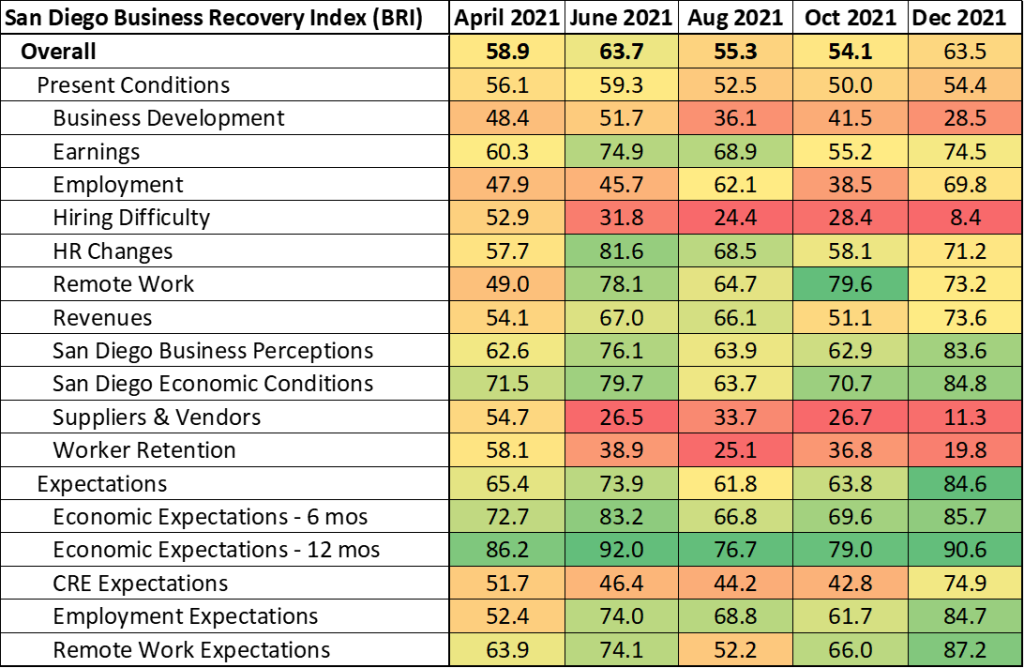

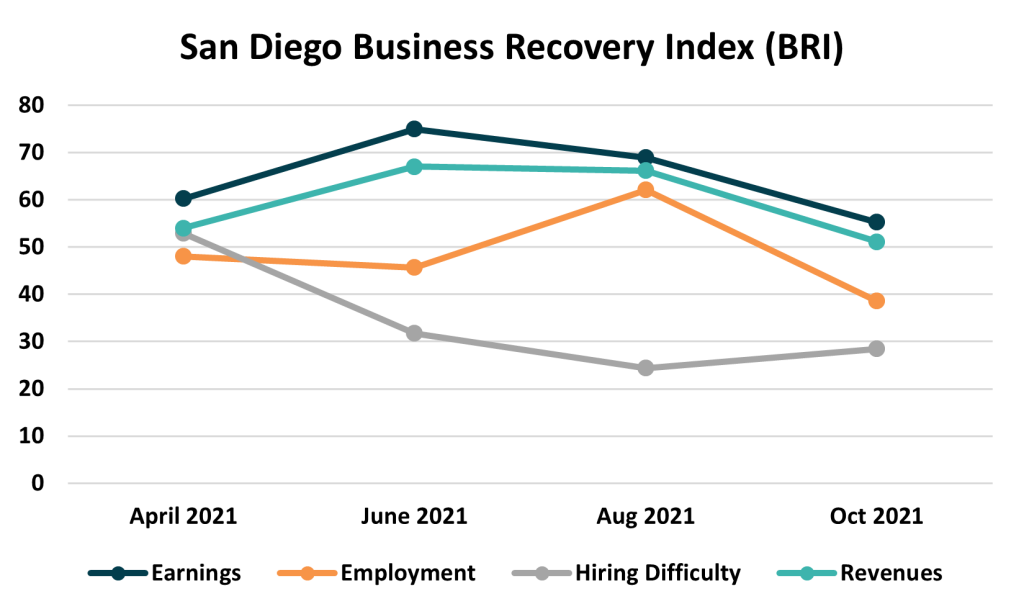

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, San Diego Regional EDC surveyed nearly 200 companies in the region’s key industries on a rolling basis throughout 2021 to monitor and report shifts in their priorities and strategies. In addition, EDC constructed the San Diego Business Recovery Index (BRI)—a sentiment index to measure companies’ perceptions of current conditions, as well as expectations for the future across several factors such as business development, employment and commercial real estate needs. (An index value >50 reflects expansion, and a value <50 reflects contraction. More information on the index and how it is calculated is available at sandiegobusiness.org/research.)

These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation, and infrastructure development. Companies are surveyed on several topics, with varying emphases in each wave.

Here are three key findings from the final wave of surveying conducted in December 2021:

Companies have settled into their pandemic modes of operation. Revenues and employment have stabilized, driving positive sentiment of San Diego’s current business environment.

Pandemic-driven challenges aren’t going away soon. Businesses report greater struggles with hiring, retention, and supply chain disruptions than at any other point in 2021.

Businesses enter 2022 with a renewed level of optimism. The challenge will be in meeting industry’s growth with infrastructure investment needed to sustain it.

San Diego businesses reported mainly positive views on both the current conditions and expectations for region’s economy during the next six to 12 months. Although there was significant variation in these sentiments depending on the size of establishment, the overall results of December’s Changing Business Landscape survey were positive. The BRI climbed 9.4 points from 54.1 in October to 63.5 in December, reflecting more positive views of current economic conditions as well as much more bullish view of the future.

Companies have settled into their pandemic modes of operation

Across firm size and industry, business perceptions are thatSan Diego’s economic engines have adapted better than peer metros in the United States during the pandemic. As new coronavirus variants continue to surface, this adaptability is paramount to the continued success of the region’s businesses, both large and small. Furthermore, businesses rated San Diego’s economic health higher in December than at any other point in the year.

The biggest driver behind the rosy views of current business conditions surrounds employment, with San Diego businesses indicating that they have significantly increased their workforce since the start of the pandemic. This is principally driven by innovation industries, such as Life Sciences and Manufacturing. Life Sciences companies, in particular, are growing rapidly, raising $5 billion in venture capital funding in 2021 alone.

Along with growing payrolls, San Diego businesses are also reporting a rebound in both revenues and earnings. However, the magnitude of the rebound varies by business size. Businesses with fewer than 50 employees reported milder up swings (BRI values in the low-50s) compared to businesses with more than 250 employees (BRI values in the mid-70s). Here again, Life Sciences and Manufacturing led the way. However, some surprising results came from Software companies which reported declines in both revenues and earnings back in October. This could also be attributable to a surge in venture funding during the fourth quarter of 2021.

Finally, business leaders appear to have adapted to the constant disruption from new coronavirus variants and we enter the third year of a pandemic. More are reporting additional changes to their human resource policies and related procedures to operate effectively, and satisfaction with remote work arrangements remains high.

Pandemic-driven challenges aren’t going away soon

The employment gains reported by companies have not come easily. Employers indicated that hiring difficulty has reached a new low with December’s BRI at a dismal 8.4, a massive drop from October’s already low level of 28.4. Not only are the region’s businesses spinning their wheels over ever-increasing difficulty hiring, but a new record rate of workers quitting across the U.S. has made the war for talent a two-front war. San Diego entered 2021 with more than 122,000 people unemployed. Over the course of the year that number has fallen by half and while there is technically surplus of workers in the region, demand for workers is even greater. In fact, during the month of December employers posted more than 158,000 unique jobs—nearly half of which are new positions. Nearly every industry is in need of more workers and the demand is translating into higher advertised salaries.

In addition to their troubles recruiting and retaining talent, San Diego businesses reported a sharp decline in their ability to manage suppliers and vendors as the global supply chain knot continues to disrupt normal business operations. These issues appear to be worse for larger companies, as they often require intermediate inputs from international vendors in larger quantities than smaller businesses, making it more difficult to find new suppliers when there is a delay in production or shipping. Despite these disruptions, San Diego’s transportation cluster continues to grow. This is important because it supports more than 90,000 local jobs while propelling San Diego’s global competitiveness.

Businesses enter 2022 with a renewed level of optimism

Businesses reported strong future expectations across every single forward-looking BRI segment in December. Notably, San Diego companies with more than 250 employees once again expect to lease or purchase additional commercial space in the next six to 12 months after expressing desires to reduce their collective footprint in October. Here again, medical device manufacturers, and manufacturers more broadly, are driving the trend. Additionally, expectations for future remote work were strongest in December by a large margin. Companies of all sizes and industry have embraced remote work, to some degree, as a part of how they operate going forward.

While the impacts of omicron are not necessarily captured during the last wave of surveying, businesses nonetheless feel that San Diego has fared well in adapting to changing regulations and continuous staffing and supply chain uncertainties. If this is, in fact, the next normal, San Diego’s economic engines are well positioned to drive that growth.

While businesses surveyed leave 2021 with a renewed sense of optimism, 2022 will bring more questions than answers. Will remote work and a continually rising cost of living begin to drive talent away? Will the ‘great resignation’ translate into surge of new startups? Will record venture capital prove to be circumstantial or drive a new Life Sciences boom? Will the billions of dollars of public funding from the state align to support growth? EDC will be monitoring these trends and how companies continue to adapt in the face of an ever-changing business landscape.

For San Diego to fully emerge from this global pandemic, it must reconcile an economic recovery that is full of contradictions. The region is simultaneously experiencing strong job growth and eye-watering venture capital investment, along with widespread labor shortages, small business closures, and a housing market that is nearly 30 percent more expensive. Moreover, these impacts were not felt evenly across the region. The brunt of the adverse health and economic impacts of the pandemic were incurred by low-income earners and people of color.

The past year was one of adaptation and endurance, but also a year that reinforced the need to focus on the fundamental building blocks of a strong economy—quality jobs, skilled talent, and thriving households. The next year will be one where resilience means connecting more people to innovation industries; competitiveness means more San Diegans have the skills the economy needs; and prosperity means that working families can afford to live here. More than ever, smart economic development means inclusive economic development.

Presented by Meyers Nave, this edition of San Diego’s Data Bites covers December 2021, with data on employment and more insights about the region’s economy at this moment in time. Check out EDC’s Research Bureau for even more data and stats about San Diego.

KEY TAKEAWAYS

San Diego’s unemployment rate dropped to 4.2 percent in December from 4.6 percent in November; the number of people unemployed is nearly half of what it was a year ago.

A banner year in venture capital funding appears to be driving job growth in Scientific Research and Development Services, which ended 2021 up 13.6 percent.

The demand for skilled workers far exceeds the current supply of talent within the region. Key positions that employers are hiring for have high salaries and educational requirements.

Job losses and lower labor force participation in December

San Diego saw its unemployment rate fall again in December to 4.2 percent, however labor force participation declined as well. Compared to December 2020,there are now 56,900 fewer people unemployed. While many have returned to work as evidenced by the strong job growth throughout 2021, more than 65,000 people continue to be out of work. The region’s unemployment rate remains below that of the state and above the national average, 5.0 percent and 3.7 percent respectively, as it has been throughout the year.

Total nonfarm employment dropped by 1,200 jobs in December. Construction and Healthcare and Social Assistance experienced the greatest monthly declines, each shedding 2,400 payroll positions. However, many of the job losses were offset by gains in other sectors. Professional and Business Services led the way with 4,100 jobs added in December and is now up 5.3 percent from December 2020. Trade, Transportation, and Utilities also increased by 2,500 jobs, driven by Retail Trade, which boosted the overall sector with 1,200 jobs.

Record venture capital funding is propelling job growth

In 2021, the region pulled in nearly $9 billion of venture funding dwarfing anything seen in years past. While the biggest venture capital deals have gone toward technology startups, San Diego Life Sciences companies pulled in $1.6 billion more than their tech counterparts throughout the year. The surge of venture capital dollars is beginning to translate into faster job growth in San Diego.

Scientific Research and Development Services added 1,700 jobs in December after averaging monthly gains of just 300 jobs during the first 11 months of 2021 and is now up 5,200, or 13.6 percent, compared to a year ago. This represents a rapid acceleration from the 7.0 percent growth rate of previous five years. Looking further back, we see that the industry has nearly doubled its contribution to the regional economy, which was slightly above $5 billion in 2010 and is now about $9.7 billion.

While an additional 5,200 jobs in a high paying industry is certainly welcome, an analysis of job postings suggests that San Diego employers were trying to hire as many as 39,000 more workers in 2021. The demand is mostly for high-skilled, high-paying positions. In fact, more than 21 percent of jobs in the industry are concentrated in just four occupations: medical scientists, biochemists and biophysicists, project management specialists, and software developers. Importantly, all these positions typically require a four-year college degree at the entry-level.

Employers have reported increasing difficulty hiring throughout the year, leaving the region woefully undersupplied in terms of the talent needed to sustain industry growth. Ensuring that the region is an affordable one is paramount to attracting and retaining talent. In the long-term, San Diego must invest in the next generation workforce and develop a pipeline of skilled talent to meet employer demand. Looking at the demographics of the region, the focus must be on an inclusive economic development strategy that support Black and Brown youth at the same level of their white peers. Doing so will safeguard the future competitiveness of the region.

Every quarter San Diego Regional EDC analyzes key economic indicators that are important to understanding the regional economy and the region’s standing relative to the 25 most populous metropolitan areas in the U.S.

EDC explains San Diego’s Q4 2021 economic data:

Key Findings from Q4 2021:

VENTURE CAPITAL: Venture capital investments are making it rain cold, hard cash in sunny San Diego. The region’s companies closed out the year with another bonanza of VC funding in Q4, totaling more than $2.6 billion across Angel, Seed, Series A, and Growth stages–just shy of the $2.69 billion in Q1. Once again, Tech was the most funded industry, raking in north of $1.5 billion, compared to $0.6 billion in Life Sciences. Surprisingly, VC in Consumer companies reached $437 million, with apparel company Vuori pulling in $400 million alone, one of the largest investments in a private apparel brand in history. All in all, total VC funding for 2021 came in at $9 billion, compared to the $5.3 billion in 2020.

COMMERCIAL REAL ESTATE: Life Sciences companies drive demand growth in commercial real estate. A record year in venture funding is beginning to manifest itself in the commercial real estate market, as current demand for lab space is 2.75 million square feet—more than triple the amount of new deliveries expected in the next year according to a market report by CBRE. Despite 4.8 million square feet of new deliveries in the industrial market, much of this was pre-leased, doing little to stop the steady decline in the vacancy rate which ended 2021 at 2.4 percent. On top of this, asking rates for low-finish industrial space were 8.8 percent higher at the end of Q4 compared to a year ago. Furthermore, increased demand for office space resulted in the third straight quarter of declining vacancy rates, with a positive net absorption of 340,000 square feet in Q4.

HOUSING: Despite slightly lower home prices, San Diego’s affordability crisis deepens. The median home price in San Diego came in at $836,700 in December 2021, $13,300 lower than the end of Q3, as year-ago home sales fell 11.2 percent. However, home prices remain 14.6 percent higher than a year ago, worsening San Diego’s affordability crisis. Simply put, the growth in housing supply is not keeping up with demand, which could have lasting impacts on the region’s capacity to compete for the talent that drives San Diego’s innovation economy.

Presented by Meyers Nave, this edition of San Diego’s Data Bites covers November 2021, with data on employment and more insights about the region’s economy at this moment in time. Check out EDC’s Research Bureau for even more data and stats about San Diego.

KEY TAKEAWAYS

San Diego establishments added 15,000 jobs to the region’s economy in November, bringing total nonfarm employment to 1,469,800. Meanwhile, the unemployment rate dropped to 4.6 percent from a revised 5.3 percent in October. Although total employment is still 45,400 lower than pre-pandemic levels, job growth is trending in the right direction.

Retail Trade showed the largest employment gains in November with 5,400 payroll positions added, which is unsurprising as local retailers prepared for the holiday season. In fact, according to Affinity Solutions, consumer spending in San Diego during November was about 20 percent greater than January 2020.

Housing affordability is a perennial issue for San Diego. Even taking geographic variation into consideration, all but one ZIP code in San Diego is unaffordable when comparing median income to average mortgage payments. High cost of living in San Diego could push away the talent that businesses need to compete both domestically and internationally.

Employment gains continue across industries

Following October’s impressive employment gain–revised to 29,100 jobs added– employers in San Diego added 15,000 payroll positions, most of which is from hiring for the holiday season. Employment in Retail Trade increased by 5,400 and was fairly consistent throughout subsectors. Despite brick-and-mortar establishments remaining open, novel variants of the COVID-19 virus remain a concern, creating hesitancy to return to work or shop in-person.

As such, e-commerce and online retail are expected to have record years, reflected in part by employment gains in Transportation and Warehousing of 2,200 jobs. Since more consumers are shopping online this holiday season than in previous years, online retailers are employing more workers in fulfillment centers and warehouses. In fact, Amazon is further expanding its footprint in the region, with a new warehouse and jobs in Otay Mesa.

Although these employment gains are often seasonal, San Diego’s thriving Life Sciences cluster is driving growth of quality jobs in Professional and Business Services, with Scientific Research and Development Services adding 700 jobs in November. These jobs are not only high-paying, but the ripple effects through the rest of the economy are significant, as every job in Scientific Research and Development Services supports two jobs elsewhere in the economy through indirect and induced effects.

Affordability remains a challenge

It is no secret that coastal regions are some of the most expensive places in the world to buy a home, and San Diego is no exception. Although the housing affordability crisis was present before COVID, the pandemic has had profound effects on the housing market. Home sales in San Diego skyrocketed across 2020 and 2021, taking home prices along for the ride to record highs. Although the determinants of this activity are many, the Great Reshuffling of workers played a large role in what the housing market has experienced over the past two years. The relocation of workers has many facets, but two stand out: workers being forced to move to a more affordable region due to being laid off; and the adoption of remote work by many employers.

As some workers were forced out of San Diego in search of employment and more affordable housing, others fortunate enough to keep their jobs in a remote work environment were afforded the opportunity to move into the region. Anecdotal evidence abounds of homes being sold in the snap of a finger, in cash, and above listing price. Over the course of the pandemic, the ratio of median home sales price to median home list price was greater than one in many ZIP codes in San Diego. This means that demand for homes was so great over the pandemic that competitive offers for purchasing a home needed to come in above the listing price.

While the sale-to-list ratio sheds light on activity in the housing market, affordability is captured by the ratio of median household income to average mortgage payments, with higher numbers implying better affordability. Generally speaking, mortgage payments should comprise about 30 percent of household income–an income to payment ratio of 3.3; any more than that is considered housing cost burdened. We calculated the average monthly mortgage payment for the median priced home in ZIP codes across San Diego, using mortgage rates provided by FRED and assuming zero percent down. Comparing the median household income in each ZIP code to these average mortgage payments gives an indication of the level of affordability in a given geographic area.

True to the trend, coastal communities in San Diego are the least affordable, with many ZIP codes showing an income to payment ratio below 1. In fact, there is not a single coastal community that exhibits an income to payment ratio above 1.4. This means that if the median income household purchased a home at the median price for that particular ZIP code, approximately 71 percent of their monthly income would be allocated toward their mortgage payment.

As can be seen in the interactive map above, the further away from the coast, the more affordable housing is relative to the coastal communities. However, this does not simply imply that housing is affordable in absolute terms. Taking an income to payment ratio of 3.3 as the threshold of housing cost burdened, only one zip code in San Diego qualifies as affordable: Palomar Mountain, 92060.

San Diego is an unaffordable market for a majority of home buyers, especially first-time home buyers who were born and raised here. The most pressing problem is the slow pace of new construction permits, which are not keeping up with population growth and housing demand in San Diego. As San Diego becomes a more expensive place to live, talent is steered away from the region. Developing, recruiting, and retaining this talent is pivotal for the success of regional businesses, both large and small.

Welcome to the fifth edition in EDC’s Changing Business Landscape Series, which will be published bi-monthly in the San Diego Business Journal and here on our blog. If you missed them, check out all past editions here.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. Companies in every industry are rapidly re-evaluating how they do business, changing the way they interact with customers, manage supply chains and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, San Diego Regional EDC is surveying nearly 200 companies in the region’s key industries on a rolling basis throughout 2021 to monitor and report shifts in their priorities and strategies. In addition, EDC constructed the San Diego Business Recovery Index (BRI)—a sentiment index to measure companies’ perceptions of current conditions, as well as expectations for the future across several factors such as business development, employment, and commercial real estate needs. (An index value >50 reflects expansion, and a value <50 reflects contraction. More information on the index and how it is calculated is available here.)

These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation, and infrastructure development. Companies are surveyed on several topics, with varying emphases in each wave.

Here are three key findings from the wave of surveying conducted in October 2021:

For software companies, the struggle is now real. They have been among the most optimistic industries surveyed, but now face similar challenges to other industries.

The market for skilled talent has never been hotter. A great convergence of talent needs is turning hiring difficulties into slower job growth.

Supply chain disruptions appear to be pinching profit margins. Input prices have risen for many companies, but most are reluctant to pass along higher costs to their customers and opting to sacrifice earnings for now.

The BRI took a step back in October to settle at 54.1, marking the second consecutive decline since June. The topline index value edged 1.2 points lower from August’s 55.3 but is 9.6 points off its June high of 63.7. The deterioration stems from weaker perceptions of present conditions, but slightly more hopeful views of the future helped keep the overall BRI in expansion territory.

Companies reported a slowing of both revenues and earnings. This comes after a period of record earnings in some industries but could also be the result of prolonged supply chain disruptions that have choked off necessary inputs and simultaneously prevented sales. Yet, businesses surveyed also expressed continued difficulty hiring and retaining workers, driving a significant slowdown in job growth.

For tech companies, the struggle is now real

Firms in industries with limited remote work capabilities, such as Healthcare and Aerospace, continued to express relatively pessimistic views. Joining this list are Information and Communications Technology (ICT) and Software companies, which up to now have been among the most optimistic industries surveyed.

Software companies signaled revenues have begun to fall, along with an even steeper decline in earnings. Supply chain disruptions play a role here, as San Diego is top 10 exporter of services. Limited availability of or access to key inputs, as well as travel restrictions, have hindered San Diego Technology companies from growing their businesses. Making matters worse, these businesses also expressed far greater difficulty finding people to hire compared to the summer months, which is driving a significant slowdown in job growth. Taken together, these headwinds led respondents to sour on the economy—both presently as well as future expectations for the next six months to a year.

ICT firms have also lost some faith in their current and future economic prospects. Companies in this vertical are facing even greater supply chain difficulties than Software firms. Business development and hiring pose far greater challenges than they did in the summer. Worse still, worker retention has become nearly impossible as a record number and a record rate of people quit their jobs in September.

The market for skilled talent has never been hotter

Talent recruitment and retention challenges have undermined employers since before the pandemic began. What is new is employers reported a sharp slowdown in job growth as workers drive a hard bargain. Not only are workers seeking higher wages and more flexible work arrangements, but employers find themselves competing across industry for an increasingly limited pool of skilled talent.

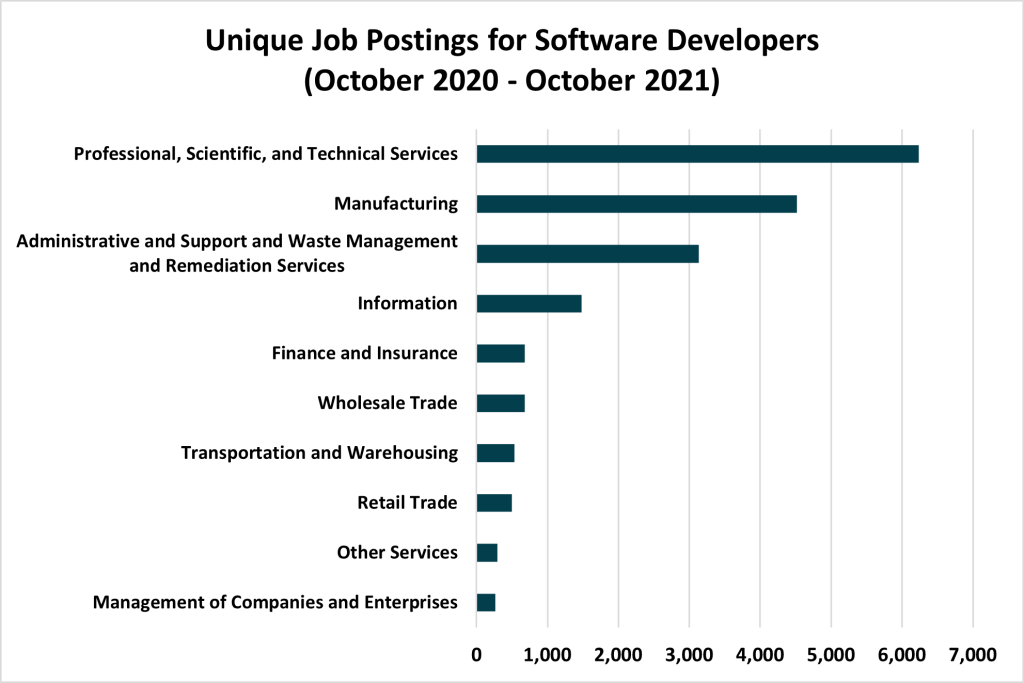

The top posted occupation in San Diego during the last year, outside of registered nurses, was for software developers and software quality assurance testers. There were more than 23,000 unique job postings for those occupations going back to October 2020. The top posting companies for these jobs are tech giants, such as Qualcomm and Apple, as well as startups receiving record venture funding. However, manufacturers comprised a formidable second with 4,514 unique positions during that time.

Manufacturing in San Diego has long been advanced—producing everything from jet engines to medical devices—so elevated demand for software developers working on unmanned aerial systems or DNA sequencing may not be all that surprising. Nevertheless, digging a bit deeper, we find the second most listed skill among Manufacturing job postings was for Teradata SQL, an open-source database management system. In fact, during the past 12 months, Manufacturing job postings that included Teradata SQL quadrupled and represent nearly 71 percent of all postings seeking that skillset. The median advertised annual salary for jobs requiring this skillset is $126,000, which is up 40 percent from a year earlier, and about $5,000 more than in either San Francisco or San Jose, and about $30,000 more than in Seattle.

The demand for skilled talent is rising rapidly and spreading across industries. Unfortunately, the supply of that talent has not kept pace. In fact, census data show an overall decline in the number of total degree holders in the region since 2017. A rising cost of living against a backdrop of increasing competition from “tech markets” across the globe poses a real challenge for local companies. With still more than 86,000 people unemployed, it has never been more important that the region invest in upskilling and building a pipeline of local talent to fuel San Diego’s recovery and future growth.

Supply chain disruptions appear to be squeezing profit margins

Supply chain disruptions and inflation continue to dominate headlines. While these challenges appear to be temporary, they are impacting consumers and the business decisions of local companies. Companies surveyed indicated supply chains are just as challenging now as they were in June. Furthermore, these challenges are directly tied to increases in input prices. This is leaking downstream into business development and sales, which employers, on balance, now rate as only slightly expansionary.

As such, some companies are considering passing along higher input costs as margins get squeezed from both sides. This decision largely depends on the magnitude of price increases that companies are facing themselves. Most companies are willing to absorb the bulk of increased costs when those increases are relatively small; tolerance for deeper margin cuts were much smaller. Only one in four companies indicated wanting to pass along at least half of those increased costs, where input prices have risen less than five percent. However, companies are nearly twice as likely (44 percent) to do so where input prices rose more than five percent—principally those in Manufacturing.

Passing along increased costs is a short-term strategy to a complex problem. As such, some companies are reevaluating their supply chains, not just in terms of suppliers but also the networks they rely upon to receive inputs or distribute products. Of the companies surveyed, only 14 percent indicated currently using the Port of San Diego. However, nearly double (27 percent) expressed a willingness to do so in the future.

The survey results continue to reflect an uneven recovery across industries. The reported trends in employment line up squarely with recent jobs reports for the region. In total, San Diego establishments added an underwhelming 3,600 jobs to the economy in September. The sharp slowdown in job growth helps explain the upward shift in remote work adoption as well as future expectations for remote work accommodations. There are many surveys of workers, both locally and nationally, indicating that desires for flexibility and remote work are strong and sticky. Despite these challenges, employers surveyed remain optimistic about the next six to 12 months albeit somewhat more modest plans for expansion.

Stay tuned for more on San Diego’s changing business landscape. EDC will be back every other month with more trends and insights. For more data and analysis, visit our research page.