Each month the California Employment Development Department (EDD) releases employment data for the prior month. This edition of San Diego’s Data Bites (formerly the Economic Pulse) covers March 2021 and reflects the lingering effects of the coronavirus pandemic on the region’s labor market. Check out EDC’s Research Bureau for more data and stats about San Diego’s economy.

Key Takeaways

- San Diego establishments added 9,900 new payroll positions in March, but gains were uneven across industries.

- The unemployment rate edged lower to 6.9 percent from February’s 7.2 percent. However, this was due primarily to the loss of 10,300 workers from the labor force.

- Consumer spending has improved significantly as households spend stimulus checks and unwind the savings accrued over the past year or so; this could mean tens of thousands of jobs in Leisure and Hospitality and Retail in the coming two to three months.

First glance

The March jobs report for San Diego was a mixed bag. Employers added 9,900 new payroll positions, and the unemployment rate edged lower to 6.9 percent from 7.2 percent in February. However, job growth was uneven across industries, with gains in Leisure and Hospitality, Professional and Business Services, and Government partially offset by declines in Construction, Manufacturing, and Retail. Moreover, 10,300 workers left the job market in March—or roughly a third of the 29,800 people who either joined or rejoined the labor force in February. In fact, it was the loss of these workers that pushed the unemployment rate lower more than employment gains.

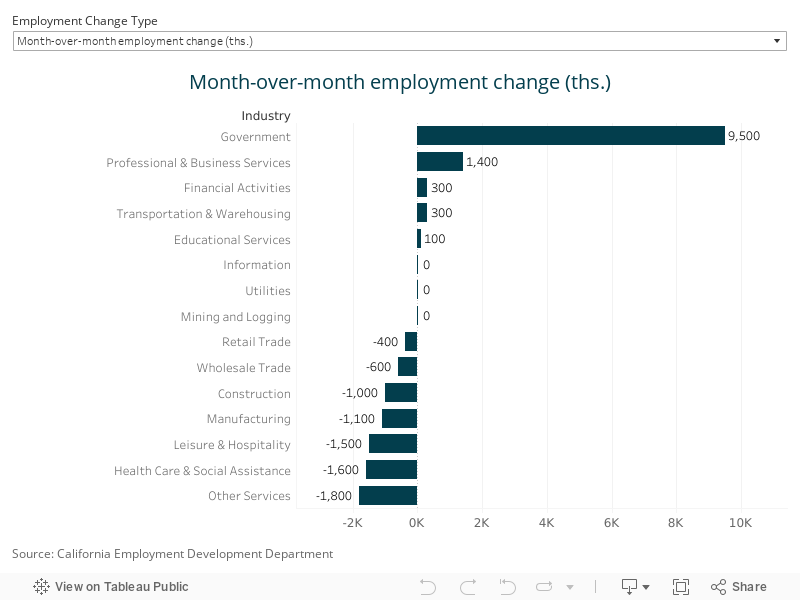

Industry view

Job gains were apparent in just nine of the 16 supersectors tracked by the EDD. This is somewhat surprising, given March’s blowout employment report for the U.S., which showed nearly a million new jobs were created.

Leisure and Hospitality establishments added 5,000 jobs in March, building on the 13,200 positions recovered in February. Also encouraging, more than half of these jobs came from restaurants. Meanwhile, Professional and Business Services logged an additional 3,300 positions thanks to a big push from the crucial Professional, Scientific, and Technical Services segment, which notched 2,900 more jobs in March than the month prior.

Builders let go of 1,500 workers in March, reversing most of the 2,100-worker gain from February. And, while losses in Construction aren’t completely unheard of in March, they’re certainly the exception rather than the rule. Builders have let go of workers in March in only seven of the past 31 years.

Manufacturing, Retail, Finance, and Real Estate companies let go of a combined 1,100 workers in March. These figures may reflect some statistical noise and potentially even some buyback after February’s strong report. Nonetheless, the loss of 400 Retail positions is a surprise, especially following the March U.S. retail sales report, which showed a huge rebound in consumer spending last month.

Relief for Hospitality and Retail is (finally) on the way

U.S. retail sales, which include sales at restaurants and bars, jumped by 9.8 percent in March, blowing past analysts’ expectations. The meteoric rise was in large part the result of stimulus payments that were distributed to millions of households last month as part of the Biden administration’s $1.9 trillion COVID-19 rescue package.

In addition to stimulus-related spending, consumers may have also begun unwinding some of their savings now that a sustained recovery appears to be in the offing. To be sure, households began hoarding cash at the onset of the downturn last year. The U.S. personal saving rate peaked at 33.7 percent last April, decimating the previous record of 17.3 percent that was set in May 1975, and remained perched at an elevated 13.6 percent in February 2021, which is nearly double the pre-pandemic average of 7.3 percent observed between 2010 and the end of 2019.

As long as the news around COVID cases continues to be positive and residents continue to be vaccinated at current rates, it’s not unreasonable to suspect that consumers will continue to spend freely into the summer and fall months.

This is particularly good news for San Diego’s restaurant and bar scene. Given the region’s status as a premier tourist destination, changes in national spending at eating and drinking establishments correlate strongly with job growth here at home. If sustained, March’s leap in U.S. retail sales could mean as many as 50,000 to 60,000 payroll positions at San Diego’s bars and restaurants, in addition to March’s jobs build as employers continue to meet rising demand.

Retailers can also expect a big boost. If historical relationships hold, 15,000 to 20,000 positions could appear in April and May if consumers continue to loosen their purse strings. The correlation between local Retail employment and national consumer spending is quite a bit looser than the relationship for eating and drinking places. However, as a point of comparison, local consumer spending data from Affinity also reveal a rebound, which reinforces the notion that job gains will continue for at least the next several months barring any unexpected hiccups.

Bottom line

Even though it wasn’t quite as strong as expected, March’s employment report is further evidence that the job market has finally turned the corner after a temporary slump in December and January. Nonetheless, it will still take some time before the damage wrought by the COVID downturn is undone. Payroll employment is still 7.2 percent below year-ago levels and 8.1 percent lower than the pre-pandemic level reached in February 2020. Moreover, the unemployment rate remains elevated, and 57,140 workers are still missing from the labor force.

All of this is to say, we should be cautiously optimistic. On balance, odds favor a strong rebound this year and into 2022, but there is still a lot of work to be done. Now, more than ever, it is necessary that we get this recovery right.

Training and upskilling will be vital for the thousands of workers whose jobs may never return. EDC’s Advancing San Diego program is facilitating this by connecting employers, educators, and students to the training and education they will need to thrive in the coming expansion. Just this week, Advancing San Diego announced its Preferred Providers of Manufacturing talent, and opened applications for small businesses seeking interns.

It will also be imperative that San Diego small businesses are connected to large buyers in order to keep remaining businesses in the region healthy and to help spur a new wave of entrepreneurship to meet the needs of San Diego’s largest institutions and employers. EDC’s Anchor Collaborative is working with large local businesses to help ensure big companies “shop local” for their procurement needs. Our research estimates that a one percent shift in procurement spending by large companies to local businesses could create thousands of new jobs in the region.

You might also like to read: