Each quarter, EDC’s Research Bureau releases its Economic Snapshot to analyze key economic indicators in San Diego’s economy. Read on as we take a closer look at how remote work trends are reshaping the workplace and the broader economy.

Remote first work

As the cost of living in San Diego continues to outpace compensation, remote work flexibility has emerged as a valuable incentive for job seekers—often, the most valuable. With San Diego median home prices reaching an all-time high of $1 million in Q3, working remotely opens affordable housing markets to employees without being limited by geographic constraints. Meanwhile, this allows employers to hire out-of-county or even out-of-state, increasing the pool of talent available to them.

Even still, employers grapple with concerns about the potential impact on employee productivity, leading to a spectrum of opinions on the efficacy of remote schedules. Yet, cutting overhead costs by adopting fully remote schedules has become an attractive possibility for firms.

SANDAG’s recent report on Remote Work Policies and Practices shows how the percentage of businesses that offer remote work options to their employees jumped from 27 percent pre-pandemic to 47 percent during, and 57 percent post-pandemic. This has had an obvious and indelible impact on commercial real estate demand.

What this means for real estate now

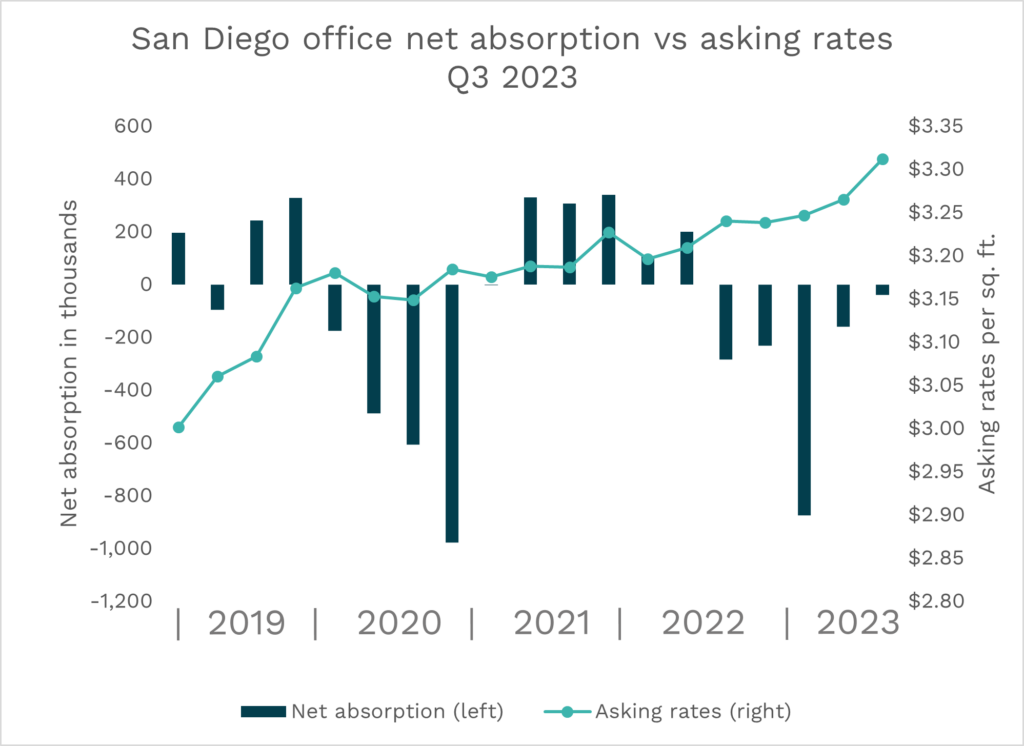

In the Q3 2023 Economic Snapshot, we saw that San Diego office real estate experienced its fifth consecutive quarter of negative net absorption, which reflects the difference between space that became physically occupied and space that became vacant. When this number is negative, it means more space became vacant than occupied during the quarter, perhaps because tenants decided not to renew leases as they became due.

San Diego’s negative net absorption trend is noteworthy for two reasons:

- Despite net absorption remaining negative for five quarters, asking rates remained at an all-time high throughout, reaching $3.31 per square foot in Q3 2023. Typically, asking rates would be expected to decrease in response to a slower demand for office space.

- Since 2010, the only other time the region has experienced five consecutive quarters of negative net absorption was during the onset of the pandemic, from Q1 2020 to Q1 2021.

Find this and other data trends in our interactive dashboard.

We know that office spaces became unoccupied during the pandemic due to public health mandates and safety protocols. But why are we seeing this trend again and what could be causing it? The answer could be observed in the previous graph, leading firms to cut office space.

While net absorption remained negative in Q3 2023, the number recovered greatly and indicated potential recovery from past quarters. In Q3, the office market experienced 37,868 square feet of negative net absorption, compared to 159,262 square feet in Q2 and 874,036 in Q1.

The negative net absorption in Q3 was primarily driven by larger office vacancies in areas such as UTC, Kearny Mesa, and Del Mar Heights, according to CBRE’s quarterly report. Similarly, the highest asking rates in Q3 were found in UTC, Torrey Pines, and Del Mar Heights. The low tenant demand and the continuing construction of office spaces combined might generate more available, yet unoccupied space.

Looking ahead and how you can get involved

As the San Diego region anticipates continued changes in commercial real estate, EDC is scoping a unique study of the local workforce in which we’ll survey the employees of large and small companies throughout the county. The first local study of scale on workforce requirements and desires (to our knowledge), our goal is to identify evolving local trends in how work is done, workers’ needs, workforce trends, and workplace requirements to inform company return to office plans as well as office tenant attraction strategies.

Updated survey work and studies combined with tools such as EDC’s Investment Map can help private and public investors better understand workforce and workplace trends when making commercial real estate development decisions that benefit both employers and workers. To get involved, contact EDC’s Senior Director of Research and Economic Development:

Eduardo Velasquez

Vice President, Economic Development & Research

You might also like to read: