Over the last several months, our work at EDC has had to move and change in some significant ways to respond to the economic conditions around us. And while this is always a part of our work and planning, it is safe to say that 2020—and the early stages of 2021—challenged us greatly and taught us a lot about our work and our economy, as it did all of you.

Investors and community partners often ask me what a day or a week at EDC looks like—some are just curious what the actual work feels like on a day-to-day basis; others are interested in knowing what we are seeing and experiencing through the businesses we work with to better understand if their needs and priorities may signal bigger or broader economic trends, challenges, or opportunities for the region.

As we kick off the third quarter of the year and begin developing new and improved programs, strategies, and focus areas to keep stride with our fast moving and re-opening economy, here’s a quick glance at EDC’s Q2 2021:

As always, we do all that we do with an eye on building a stronger, more inclusive economy, producing more skilled workers, creating more quality jobs within our small businesses, and establishing more thriving households and a better quality of life for businesses and residents in all corners of the San Diego region. We truly could not do any of it without you, and we thank you for your continued investment, leadership, and support.

Welcome to the third edition in EDC’s Changing Business Landscape Series, which will be published bi-monthly in the San Diego Business Journal and here on our blog. If you missed them, check out the March and May editions.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. Companies in every industry are rapidly re-evaluating how they do business, changing the way they interact with customers, manage supply chains, and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

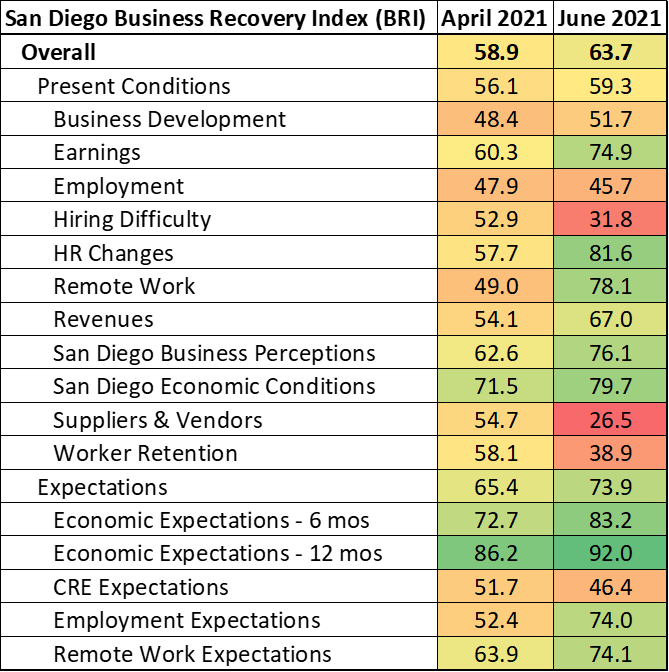

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, EDC is surveying more than 200 companies in the region’s key industries on a rolling basis throughout 2021 to monitor and report shifts in their priorities and strategies. In addition, EDC constructed the San Diego Business Recovery Index (BRI)—a sentiment index to measure companies’ perceptions of current conditions, as well as expectations for the future across several factors such as business development, employment and commercial real estate needs. (An index value >50 reflects expansion, and a value <50 reflects contraction. More information on the index and how it is calculated is available here.)

These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation, and infrastructure development. Companies are surveyed on several topics, with varying emphases in each wave.

Here are three key findings from the third wave of surveying conducted in June 2021:

We are amid a great talent reshuffling. Businesses report increasing difficulty hiring and retaining talent, meanwhile the quits rate is at historic highs.

Supply chains remain knotted up. The strategic importance of our cross-border trade has never been clearer.

Space needs are in flux as companies prepare for return to office. Demand for office space may be waning, but life sciences companies are looking to add lab space.

San Diego County firms built on the enthusiasm expressed in April’s survey, with the BRI advancing from 58.9 in April to 63.7 in June. The topline index was pulled higher by more upbeat views of, both, present conditions and expectations for the future. The present conditions index segment rose from 56.1 in April to 59.3 in June while the expectations segment climbed from 65.4 to 73.9 during that time. Business respondents in the region confirmed several trends that have made headlines recently. Companies stated that business conditions have improved significantly over the past two months (due in no small part to California’s reopening in June) while also noting that sourcing talent and suppliers has become significantly more difficult.

A great talent reshuffling

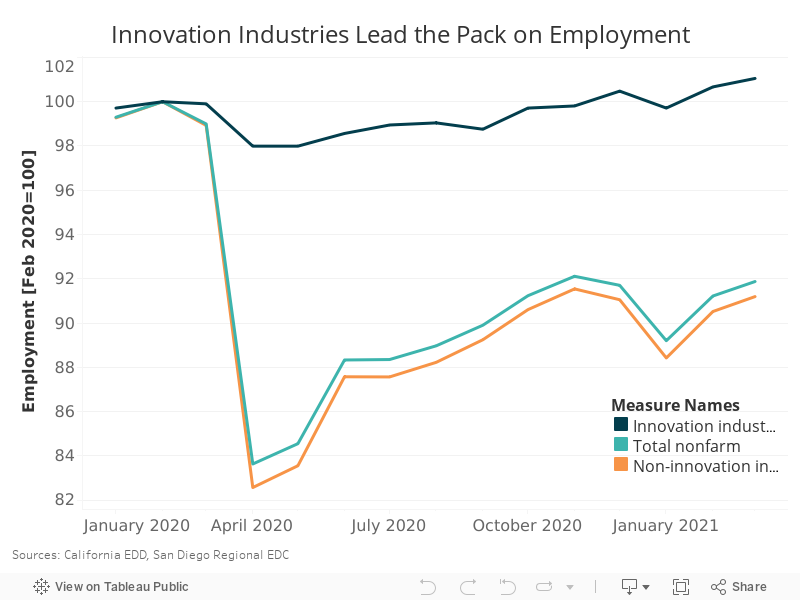

Companies reported that revenues and earnings have improved since April and thus optimism over the next six to 12 months has increased. Expectations are also strong in San Diego’s Innovation cluster. Businesses in this group conveyed that they plan to hire more aggressively in the coming months. This is particularly good news, since each new Innovation job supports another two jobs elsewhere in the regional economy.

Nonetheless, companies also reported having a tougher time attracting new talent as well as increased difficulty retaining existing workers. There has been much ado about labor shortages and the impact of increased and extended unemployment benefits, but the data show that there is a much more nuanced story. First, there is a large mismatch between the talent in-demand and the talent available to work. As of May (most recently available data at time of writing), there were 104,400 people unemployed in the San Diego region and more than 115,000 job openings. However, the top hiring industries are Administrative and Support Services, Professional Services and Manufacturing industries (nearly 40 percent of unique postings), whereas the bulk of the unemployed come from Leisure and Hospitality.

Second, there are record numbers of workers quitting their jobs. The Bureau of Labor Statistics measures the proportion of workers who voluntarily leave their job relative to total employment. This “quit rate” sat at 2.5 percent in May 2021 after falling from 2.8 percent in April—the highest ever recorded. The Conference Board survey’s labor market differential, another measure of views on whether jobs are plentiful or hard to get, vaulted from 36.9 in May 2021 to 43.5 in June. That is the highest level since 2000.

All this quitting not only reflects confidence in the availability of work, but also the changing needs and desires of workers. The San Diego Association of Governments surveyed both employers and employees earlier this year and found that only 36 percent of employers expect to have one or more employees working from home at least one day per week. Meanwhile 44 percent of employees surveyed expect to work from home an average of 1.2 days per week. This difference in expectations partly reflects differences in opinion of how remote work has impacted productivity—only nine percent of employers reported increased productivity during the pandemic versus 48 percent of employees.

Flexibility will be key to keeping and attracting the best and brightest of workers. Perhaps the companies EDC surveyed understand this better than most, as they indicated both improved efficiencies from, as well as increased planned future utilization of, remote work technologies in June compared to April.

Investing in supply chains locally, binationally

Hiring challenges are also impacting supply chains globally. Companies reported a sharp decrease in the accessibility and reliability of their suppliers and vendors. Here, BRI fell from 54.7 in April to a categorical low of 26.5 in June. This corroborates the headlines regarding shortages in lumber and microchips, which has in turn stalled production of higher end goods and led to spikes in commodity prices and other item such as used cars. A lot of these supply chain disruptions are temporary in nature, directly linked to safety measures and restrictions associated with pandemic (this is why longer-term inflation expectations remain stable).

Ports and businesses across the country have experienced ongoing shortages of labor, containers, truck chassis, and more; shipping vessels have been forced to wait in harbors, in some cases for more than two weeks. This global traffic jam has impacted schedule reliability so profoundly it has forced companies to revisit the ways in which they manage risk. Many companies have moved from a just-in-time strategy to just-in-case. This means firms now keep additional inventory on hand, anything from raw materials to the final product. The lack of supply and rising costs have disproportionately impacted small and mid-market suppliers and buyers. This has resulted in direct capital investment from smaller buyers into smaller suppliers to stabilize supply chains and build necessary redundancies.

The pandemic-induced constraint on the movement of goods has only exacerbated trends from the past few years. Trade wars, changing consumer behavior, and e-commerce were already disrupting global supply chains, all of which has highlighted the strategic importance of supply chain management as well as the region’s bi-national assets. The Cali Baja Binational Mega Region is already vertically integrated in Manufacturing, and a warehousing boom in Otay Mesa is increasing capacity for goods coming via land and sea. Cali Baja is an ideal location for companies that want to move operations closer to home but maintain a binational advantage. Continued investment in trade infrastructure, such as our ports of entry and direct route service, will further cement Cali Baja as a binational innovation hub.

The return to office will be in a lab

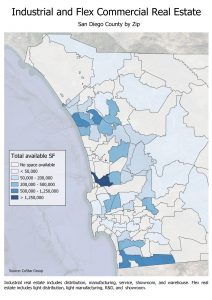

Back in April, companies indicated a modest desire to increase their physical footprint upon returning to the office. However, companies appear to be less sure as the return approaches. In June, companies expressed plans for a net reduction of space, but a deeper dive into the responses reveals that it is demand for office space that is waning. In fact, there is increasing demand for commercial space—life sciences companies in need of laboratory space. This reflects the influx of investment and rapid hiring we are seeing in these industries, as they lead the fight against the global pandemic. Fortunately, there is nearly 10 million square feet of industrial and flex space across San Diego County currently available for lease or purchase that could potentially accommodate this demand. Current hot spots include Sorrento Valley, Vista, and Otay Mesa; Downtown San Diego is also building capacity rapidly.

The headline story is a positive one for San Diego’s economy, but sentiment is far from identical across business sizes and industries. For example, small companies with fewer than 50 workers logged BRI of 53, which is modestly in expansionary territory, while companies with 250 or more employees measured an index value of 63.7. This makes sense, because San Diego’s Leisure and Hospitality businesses tend to be smaller establishments and were the hardest hit during the pandemic. While companies are enthusiastic to get back to full capacity and add workers, it will likely take a few more months for supply chains and the labor market to normalize again. The pandemic is a generational disruption with widespread ramifications, accelerating several trends already underway, including how and where people are willing to work.

Stay tuned for more on San Diego’s changing business landscape. EDC will be back every other month with more trends and insights. For more data and analysis visit: sandiegobusiness.org/research.

Presented by Meyers Nave, this edition of San Diego’s Data Bites covers June 2021, with data on employment and more insights about the region’s economy at this moment in time. Check out EDC’s Research Bureau for even more data and stats about San Diego.

KEY TAKEAWAYS

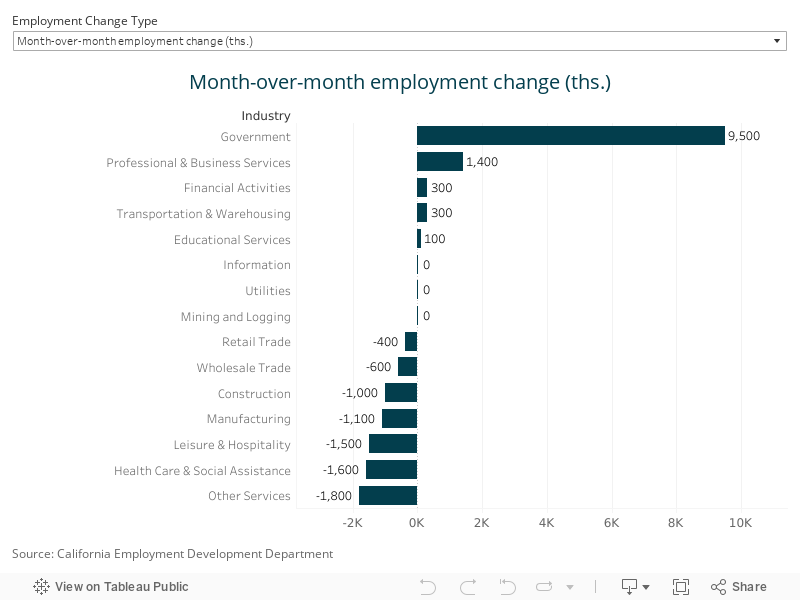

San Diego establishments added a middling 5,700 net new payroll positions in June, although revisions uncovered an additional 1,000 jobs in May. Gains in Leisure and Hospitality, Manufacturing, and Healthcare were largely offset by losses in Government, Professional and Business Services, Education, and Finance.

The unemployment rate unexpectedly jumped to seven percent from May’s 6.3 percent, according to a separate survey of household employment. However, this was driven in large part by 7,600 people either joining or rejoining the labor force last month, a positive sign for future growth.

Data suggest that enhanced unemployment benefits are not preventing workers from finding and taking jobs in San Diego.

First impression

San Diego establishments added a middling 5,700 net new positions in June, following a build of 3,000 (initially reported as +2,000) jobs in May. Leisure and Hospitality continued to lead gains with an additional 4,800 jobs last month, followed by Manufacturing (+2,000) and Healthcare and Social Assistance (+1,500). However, gains in those industries were largely offset by losses in Government (-1,600), Professional and Business Services (-800), Education (-500), and Finance (-500).

More surprisingly, the separate household survey indicated that the unemployment rate jumped from May’s 6.3 percent (initially reported as 6.4 percent) to seven percent in June. However, this was driven in large part by 7,600 people either joining or rejoining the labor force. This could prove to be a big positive for growth in the coming months, particularly since employers have been worried that there aren’t enough workers to fill open positions (more on that below).

The relatively ho-hum jobs report for last month may be a result of timing. The California Employment Development Department (EDD) surveys businesses and households during the week of the 12th of each month. However, California’s economy, including San Diego, didn’t reopen fully until the June 15, so jobs created after reopening may not show up until July’s employment report.

Are unemployment benefits preventing workers from finding jobs?

Nationally, a fiery debate has erupted regarding jobless benefits and the jobs recovery. On one side, many argue that unemployment insurance benefits, particularly enhanced federal unemployment benefits that came online as the pandemic bore down on the economy last year, are essentially “paying people to stay home” and preventing them from returning to work. Others argue that the story is more nuanced, and that other factors like access to childcare and health concerns have prevented many folks from returning.

So, what do the data tell us about San Diego’s job market?

To begin with, nearly 8,000 people entered or reentered the labor force last month, so it doesn’t appear that workers are waiting on the sidelines.

Also, job openings in the San Diego regionare on the rise and, in June, nearly matched their July 2019, pre-pandemic peak. More than 116,000 new jobs were posted last month, up 55 percent from April 2020’s nadir.

It’s important to note that, just like workers, jobs are not identical, so it’s crucial to understand which positions are being advertised and for which industries. Of the 248,000 jobs lost in the region between February and April 2020, 53 percent were in Accommodation and Food Services; Arts, Entertainment, and Recreation; and Retail. Unlike total job postings, which have essentially returned to pre-pandemic norms, postings in these three industries still rest 23 percent below their July 2019 peak. Moreover, postings in these industries only accounted for 13.6 percent of all new job openings from April 2020 to June 2021. This implies that the majority of job postings growth has been within industries that suffered far fewer job losses in the pandemic and therefore have fewer available workers to choose from, which better helps to explain why unemployment has not fallen faster in recent months.

Timing should also be considered. Leading up to the pandemic, it took a median 37 days for Accommodation, Arts, and Entertainment, and Retail companies to fill open positions. By June 2021, that number fell to 33 days (also challenging the claim that workers are engaging less with open jobs because of unemployment insurance payouts), but it still implies that it could take at least one to two months before those filled positions show up in the employment data.

Finally, of the more than 140,000 jobs recovered between April 2020 and June 2021, 85,500—or 61 percent—have come from Accommodations, Arts, and Entertainment, and Retail.

Taken together, the data suggest that workers in San Diego are eager to return to work and reestablish some sense of normalcy after more than a year of being dislocated. All told, worries over enhanced jobless benefits preventing people from taking new jobs appear to be overblown, at least locally.

As I write this, it is hard for me to believe that we are over halfway through June and summer is just around the corner.

Despite the State of California “reopening” last week, I think I have accepted the fact that things will not truly be back to normal for a very long time; yet at the same time, we see signs all around us that the way of life we all knew before the pandemic is starting to resume. In the months ahead, Team EDC will begin returning to the office much more regularly. We are starting to attend more and more in-person meetings, although the outdoor variety remains the standard. We have even put a date on the calendar for our 2022 Annual Dinner—hopeful that the year ahead continues to bring us all closer to where we once were.

While numerous things have changed about our work at EDC, the goals that we set for 2030 remain unwavering. The need to develop more quality jobs within our small businesses, more skilled workers, and more thriving households across San Diego has only become more prominent. Now more than ever, these goals must be our guideposts in re-establishing San Diego’s economic resiliency, growth, and well-being.

Committed to getting this recovery right, we have recently teamed up with local tech startup GoSite to offer up to 100 small businesses with the digital tools needed to weather future economic shocks—at no cost to them.

We know the pandemic spurred the closure of nearly 40 percent of San Diego’s small businesses—which can largely be attributed to businesses’ inability to quickly pivot online, depriving them of access to customers and key markets. We also know those hardest hit by the pandemic have been communities of color who are being left further behind. The San Diego Business Hub is one step toward ensuring San Diego businesses most impacted* by COVID-19 have the tools necessary to recover, grow, and thrive.

We feel certain that if we can support 100 more small businesses in developing the online presence they need for resiliency and growth, it will support our broader effort of increasing the number of quality jobs and thriving households within the region. And everything we do in the months ahead must ensure we are continuously taking steps in this direction. Learn more about the program at SDbizhub.com, made possible by grants from The San Diego Foundation and Union Bank.

With respect and gratitude,

Mark Cafferty

Mark Cafferty

President & CEO

*Priority applicants include women, minorities, veterans, and other economically under-resourced groups.

Presented by Meyers Nave, this edition of San Diego’s Data Bites covers May 2021, with data on employment, housing, and more insights about the region’s economy at this moment in time. Check out EDC’s Research Bureau for even more data and stats about San Diego.

KEY TAKEAWAYS

San Diego establishments added just 2,000 net new payroll positions in May. Gains in Leisure and Hospitality were largely offset by losses in Construction and Professional and Business Services.

The unemployment rate fell to 6.4 percent from April’s 6.7 percent even as several thousand people joined or rejoined the labor force.

The sharp rise in home values appears to be over, but housing affordability is still well below pre-pandemic levels.

Industry view

Job gains were inconsistent across industries. Out of the 16 supersectors tracked by the California Employment Development Department (EDD), six sectors showed job growth, three sectors showed no change, and seven sectors showed job losses. Leisure and Hospitality led these sectors with 3,900 jobs added in May—3,100 of which were in the Accommodation and Food Services subsector—tacking on to the 7,000 jobs added in April. These gains were followed by increases in Government positions (1,200 jobs), Healthcare and Social Assistance (1,000 jobs), and Transportation and Warehousing (800 jobs).

Job losses in several industries countered some of the growth in May’s employment. Professional and Business services backtracked in May with a decrease of 2,500 jobs—2,100 of which were in the Administrative and Support Services subsector. Construction also reversed some of the headway made in April with a loss of 1,200 jobs in May.

While May’s employment report may have underwhelmed, year-over-year (YoY) growth continues to show just how far San Diego’s regional economy has come since the pandemic eliminated more than 200,000 jobs in the region. Employment in Clothing and Clothing Accessories Stores has increased 136.7 percent since May of last year, followed by growth of 44.3 percent in Leisure and Hospitality. See below for month-over-month and year-over-year change by industry.

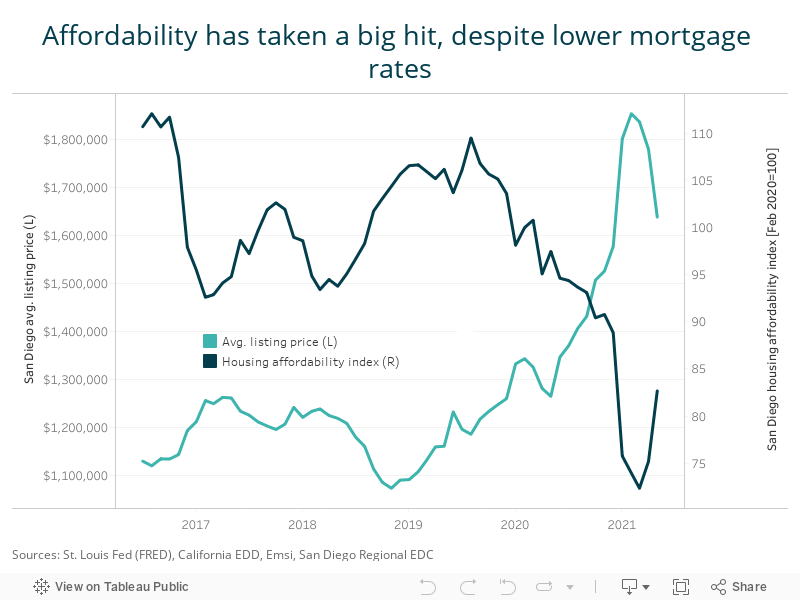

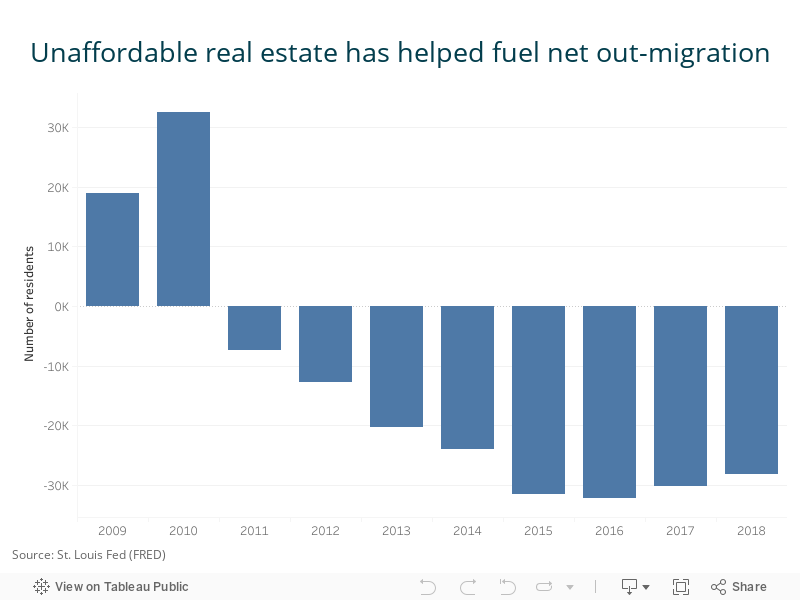

San Diego’s housing market comes back to earth, but remains largely unaffordable

Despite the unprecedented disruption to the regional labor market from COVID-19, house prices climbed at an accelerated rate. The average listing price for a home in San Diego climbed 38 percent from February 2020 to February 2021. Home values have fallen off those recent highs, but the fact remains that the average price of a home in May was still some 22 percent higher than it was in February 2020.

Fortunately, it looks like affordability (measured as the ratio of total income to average monthly mortgage payment) may be improving. After 13 months of deterioration, the aggregate affordability of a home in San Diego was up 14.3 percent in May from March 2021. Several factors are at play. First, wage income has increased as job gains have continued. Second, the rise in mortgage rates of 25 to 30 basis points has pushed home prices down to help lower average monthly mortgage payments by 12.1 percent. This is because lower mortgage rates are an important factor driving price gains for real estate in San Diego County. Mortgage rates account for 70 percent of house price changes locally, almost double the national average of 35 to 40 percent. This makes sense, considering that San Diego real estate isn’t cheap, and homebuyers have likely been trying to maximize the amount of house they can buy given their budget.

The progress on affordability is encouraging, but more work needs to be done. San Diego County’s housing market has been chronically undersupplied for more than a decade, putting upward pressure on prices. This has accelerated churn in the local population, where lower-income households are being priced out to other parts of the state or elsewhere across the U.S., but new residents are showing up with high-paying jobs in hand who can continue to drive real estate values higher. If it continues, this trend may only serve to exacerbate San Diego’s affordability problem and could limit homeownership to an even smaller proportion of the population. Ensuring San Diego remains affordable and attractive to business and people is critical to its economic recovery and future competitiveness.

Each month, the California Employment Development Department (EDD) releases employment data for the prior month. Presented by Meyers Nave, this edition of San Diego’s Data Bites (formerly the Economic Pulse) covers April 2021 and reflects the lingering effects of the coronavirus pandemic on the region’s labor market. Check out EDC’s Research Bureau for more data and stats about San Diego’s economy.

Key Takeaways

San Diego establishments added 9,800 new payroll positions in April, with most industries adding jobs over the month, but March’s employment figure was revised lower by 2,500 positions.

The unemployment rate edged lower to 6.7 percent from March’s 6.8 percent. However, this was due primarily to the loss of 16,500 workers from the labor force.

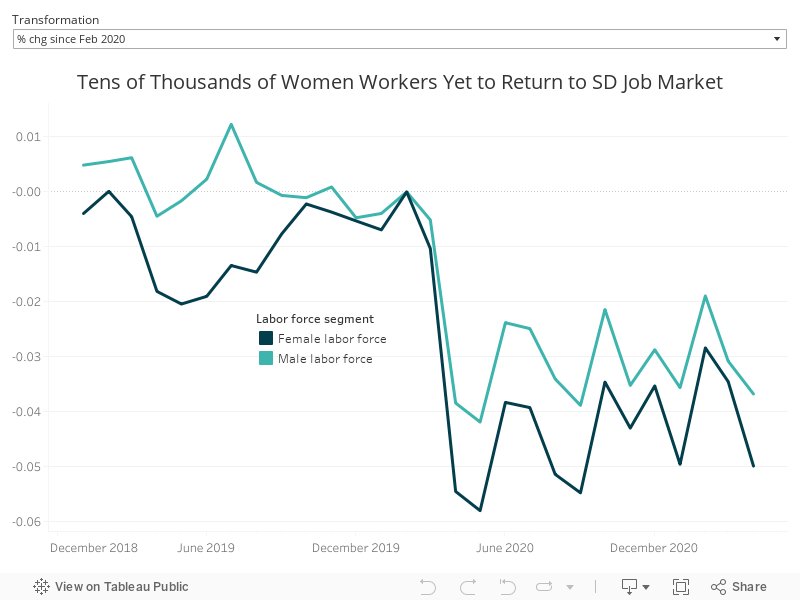

The flood of women workers exiting the labor force could reverse progress made on gender pay gaps and prolong the recovery.

First impression

The April employment report for the San Diego region was mixed. On the bright side, employers added 9,800 positions last month across a majority of industries, and the unemployment rate edged lower to 6.7 percent from March’s 6.8 percent. However, it was the loss of 16,500 workers from the labor force, not job gains, that lowered the unemployment rate. Moreover, March employment was revised lower by 2,500, reducing the initially reported gain of 9,900 payroll positions to 7,400.

Industry view

The battered Leisure and Hospitality sector led gains with 7,000 new positions, followed by 3,300 more jobs in Construction. Meanwhile, Healthcare and Social Assistance logged another 1,700 jobs, while Other Services—which include gyms and salons, among others—gained 1,600 positions over the month.

The loss of 3,500 Administrative and Support Services jobs weighed on growth in the Professional and Business Services cluster last month. Even so, Professional, Technical, and Scientific Services added 1,500 jobs and Management positions held steady. Elsewhere, San Diego’s Transportation sector lost 1,600 jobs.

The story for year-over-year growth has changed dramatically in the past two months. The jobs numbers for April 2021 show Total Nonfarm employment is 10.4 percent above April 2020 levels, when San Diego was in the throes of the pandemic. Payroll employment at clothing stores is up by more than 158 percent from a year prior while employment at restaurants is up an impressive 60.8 percent.

Fewer female workers could prolong (or even jeopardize) the recovery

Nationally, it has been widely reported that women have left the workforce in droves since the pandemic began. According to the U.S. Bureau of Labor Statistics (BLS), the female labor force participation rate declined from 57.9 percent in February 2020 to just 54.4 percent in April 2020, representing the weakest participation for women since 1986. By comparison, the rate for men declined from 69.0 percent to 65.9 percent during that time period.

Labor force participation for women has recovered somewhat since bottoming in April 2020 but has vacillated at roughly 56 percent for the past year, well below the pre-pandemic peak of almost 58 percent. The BLS estimates that some 2.4 million women are yet to rejoin the labor force, representing five percent of all female workers.

California EDD does not provide separate labor force statistics for men and women. However, assuming a similar U.S. trend has played out in San Diego, there still may be as many as 35,000 to 40,000 women still missing from the regional pool of workers. This is compared to just over 30,000 male workers who are yet to come back.

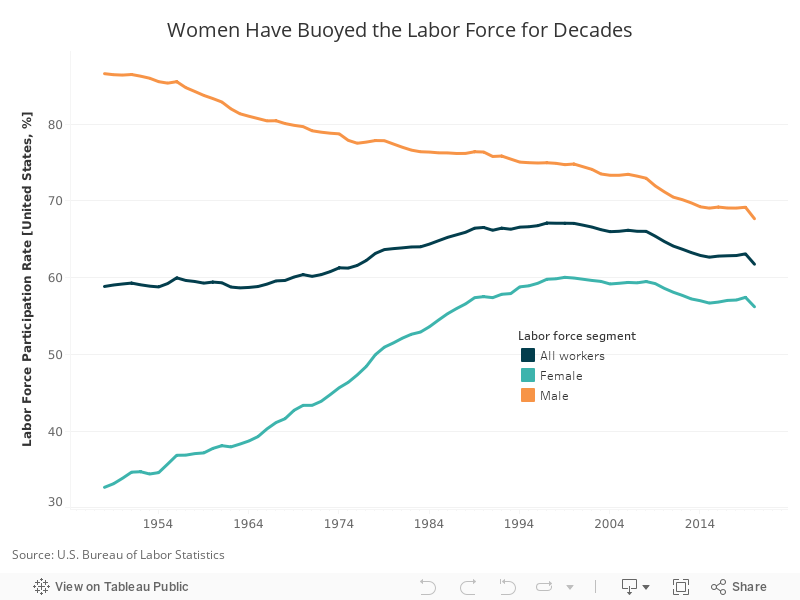

There are two key reasons why female labor force participation has dominated the headlines in recent months. First, it may erode some of the progress made on the gender pay gap. Second, women workers have historically helped to replace men as they dropped out of the labor force; nationally, female labor force participation rose from just 30.7 percent in 1948 to 57.9 percent in February 2020 as male labor force participation declined from 88.7 percent to 69.0 percent during that time.

Unpacking these points, employers are inclined to pay workers less who have been on hiatus for an extended period than workers who never left the workforce. This is because it is widely assumed that some skills erosion may have occurred during that time. This could mean a smaller paycheck for a larger number of women workers than men once (or if) they return to the labor market in the coming months or years.

Since a larger swath of the female population has left the workforce than men, this could put measurable downward pressure on average pay for women workers, thereby reversing some of the progress made in closing the gender pay gap in recent years. Worse, if pay is adjusted too much lower for female workers, then it may dissuade them from returning at all. And, while the same could be said for men, males tend to be far more likely to be employed in high-paying innovation industries, thereby mitigating the risk that men will choose not to return.

The addition of female workers over the past 60 to 70 years has also helped to stabilize the broader economy as more men dropped out of the labor force. Gross Domestic Product (GDP) can be conceptualized in a variety of ways. One way to estimate GDP growth is to calculate the sum of labor force growth and productivity growth. Through this lens, we can see that a contracting labor force is a significant drag on GDP growth. Given that men have consistently left the workforce since the late 1940s, future growth will hinge on women workers continuing to take their place. Otherwise, the U.S. economy—and San Diego’s—will have to rely exclusively on productivity gains to drive overall growth, an especially risky gamble since productivity growth has slowed immensely in recent decades.

Granted, the estimates provided above are based on national figures. But, even if the dynamics have played out somewhat differently here than across the rest of the country, we need to ensure steady engagement of our women workers. It is not an exaggeration to say that our regional economy depends on it.

Public-private partnership offering subsidized digital tools for small, diverse businesses

Today, in partnership with local tech company GoSite, EDC launched the San Diego Business Hub, which in its first phase will offer up to 100 small, service-based businesses a full suite of digital tools at no cost. Made possible by grants from The San Diego Foundation and Union Bank, SDbizhub.com is accepting applications from businesses most impacted by the COVID-19 pandemic—women, minorities, veterans and other economically under-resourced groups.

The pandemic accelerated the digital transformation of companies of all sizes and industries by as much as five years in a 12-month period, with many struggling to keep up. Since the start of 2020, the region has seen nearly 40 percent of its small businesses close. Many of these closures can be attributed to businesses’ inability to quickly pivot online, depriving them of access to customers and key markets.

We also know those hardest hit by the pandemic have been communities of color who are being left further behind in San Diego’s economic recovery.

The proof is in the numbers:

Despite making up just 30 percent of the local population, Hispanic and Latinx communities accounted for well over half of all regional COVID-19 cases and two in five related deaths.

Additionally, people of color are overrepresented in local industries that were hardest hit during the pandemic (e.g. Hispanics make up 39.8 percent of Hospitality staff and 41.8 percent of Retail staff). As a result, unemployment and loss of income have been concentrated within Black and Brown communities.

The cohort of 100 service-based businesses (e.g. personal care services, transportation, food service, home repair, small contractors, etc.) will receive GoSite’s web-based tools—which payment and invoicing, bookings, review management, customer communications, template websites and more—free of charge for one year.

Thoughts from local leaders:

“Small businesses employ the majority of San Diegans, and it’s essential we invest in their growth, recovery and resiliency if we are going to get this recovery right. This partnership with GoSite allows us to do just that: Provide the digital tools small businesses need to weather future economic downturns,” said Nikia Clarke, Vice President of Economic Development, EDC.

“This partnership is a prime example of how San Diego public, private and civic sectors rally together to solve hard problems. Access to these digital tools will help our region achieve a more equitable recovery and help small businesses struggling today be more resilient as San Diego gets back on track and back to work,” said San Diego Mayor Todd Gloria.

“Small businesses face great challenges, made worse by the COVID-19 pandemic. GoSite’s mission is to help small businesses adapt and succeed, with technology in hand for them to easily communicate with customers, manage online bookings, accept online payments, generate invoices and drive reviews—all in one place,” said Alex Goode, CEO of GoSite. “GoSite is proud to partner with EDC to create the SD Biz Hub and deliver innovative technology resources to San Diego, the place we call headquarters and home.”

“To build long-term economic resilience, San Diego’s small businesses must have resources to sustain their connections to customers and markets,” shared Mark Stuart, President & CEO of The San Diego Foundation. “This is an inspiring example of government, philanthropy and nonprofit sectors coming together to help the small businesses in our neighborhoods survive, recover and grow.”

FAQ and applications are now live, and will remain open until the cohort is full.

Welcome to the second edition in EDC’s Changing Business Landscape Series, which will be published bi-monthly in the San Diego Business Journal and here on our blog. If you missed the first edition, read it here.

Surveying the changing business landscape in San Diego

The COVID-19 pandemic has impacted every facet of life, including how businesses operate. Companies in every industry are rapidly re-evaluating how they do business, changing the way they interact with customers, manage supply chains and where their employees are physically located. This has massive immediate and long-term implications for San Diego’s workforce and job composition, as well as regional land use decisions and infrastructure investment.

To identify evolving trends in local business needs and operations, ensuring their ability to grow and thrive in the region, EDC is surveying more than 200 companies in the region’s key industries on a rolling basis throughout 2021 to monitor and report shifts in their priorities and strategies. In addition, EDC constructed the San Diego Business Recovery Index (BRI)—a sentiment index to measure companies’ perceptions of current conditions, as well as expectations for the future across several factors such as business development, employment and commercial real estate needs. Review the BRI concept and methodology here.

These insights will help inform long-term economic development priorities around talent recruitment and retention, quality job creation and infrastructure development. Companies are surveyed on several topics, with varying emphases in each wave.

Here are three key findings from the second wave of surveying conducted in April 2021:

The worst of the pandemic is behind us. Companies are very bullish about the next six to 12 months and, as a result, plan to accelerate hiring.

San Diego’s innovation cluster is (mostly) booming. Life Sciences companies lead the way while Cyber and Aerospace firms are still working through pandemic-related challenges.

Companies are seriously reevaluating their space needs. Smaller firms are looking to expand their footprint, while traditional Tech companies may be scaling down.

The worst is behind us

San Diego companies indicated that they think the worst of the pandemic has passed. With a BRI of 58.9 in April, regional firms noted that they plan to hire or rehire workers at a slightly faster pace than they have up to this point, while also expanding remote work capabilities going forward.

Last month’s index reading reflects bullish assessments of, both, present conditions (the present conditions subindex registered a value of 56.1) and expectations for the future (subindex of 65.4). Companies noted some lingering effects from a full year in lockdown, including difficulties with business development and job losses, and neutral to slightly negative feelings on remote work over the past year. Nonetheless, firms reported bright views on the current state of the regional economy and noted that San Diego businesses and key industries have adapted to the pandemic better that those in peer regions.

Regional companies were even more upbeat when it came to expectations for the future. All of the index’s expectations subindex values were north of 50, and companies overwhelmingly believe that the regional economy will have improved significantly in the next six months (subindex of 72.7) and even more so within the next 12 months (subindex of 86.2). This is important because many companies make decisions today based on their assessments of business conditions in the near future.

Most companies shared in the optimism, but to varying degrees. Small companies with fewer than 50 employees that were hardest hit during the pandemic held slightly dimmer, though still generally positive, views than their larger counterparts. In particular, smaller firms cited ongoing difficulties accessing new customers, managing suppliers and vendors, and hiring and retaining workers. Even so, assessments of current earnings trends were only slightly negative, and small firms held a sunny disposition when it comes to the current state of the San Diego economy and business climate.

Interestingly, however, companies with fewer than 50 workers had the highest level of optimism for the future across business size cohorts, which could signal an inflection point for the pace of hiring in the coming months. This bodes especially well for the jobs recovery heading into the second half of 2021, as 96 percent of San Diego’s businesses have fewer than 50 employees and small businesses have historically accounted for roughly half of all job growth.

San Diego’s innovation cluster is (mostly) booming

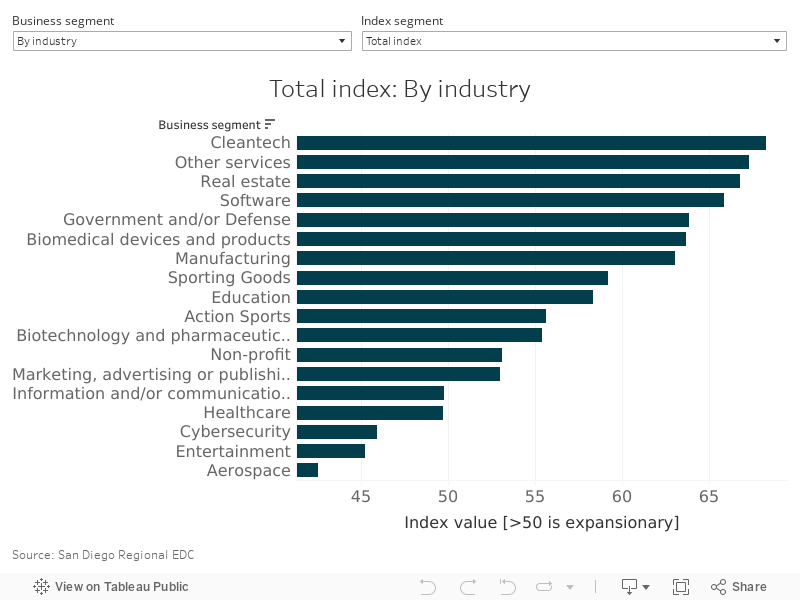

San Diego’s innovation cluster overwhelming expressed optimism entering 2021, as companies shifted toward meeting the demand for life-saving technologies, treatments and personal protective equipment leading to record venture capital investment and renewed job growth. However, a closer look reveals mixed results within the cluster. Industries like Cleantech, Software and Biomedical Device producers all held especially confident views (BRIs in the mid-60s), while Telecommunications, Cybersecurity and Aerospace each signaled ongoing challenges from the pandemic (BRIs ranging from 43 to 50).

Biotech and Biomedical Device manufactures hold strong expectations for the regional economy, with plans to increase their headcount and real estate footprint during the next year. In addition, they expect to increase their use of remote work over the same time frame. While this may seem contradictory, it reflects the modifications and enhancements that many companies are making to protect workers on the production floor, as well as those necessary to attract workers back into the office. Workers want to feel safe once back on company property and they also want to maintain the flexibility that working remotely has provided. To accommodate these needs, employers are preparing for a flexible or hybrid workplace once reopen. In addition, many companies are reconfiguring and even seeking new space to keep workers spread out, adapting space to be more comfortable in a post-pandemic environment. This includes ‘hoteling’ and ‘neighborhooding’ models to help reduce the flow of people and simultaneously allow teams to collaborate in person. Companies are preparing for a gradual return to the office to give workers adequate time to warm up to pre-pandemic routines. More on that below.

While Telecommunications and Cybersecurity firms all share this optimistic regional economic outlook with their Life Sciences peers, these industries are much more subdued about their own expansion plans for the next year. On net, they see their needs for space as unchanged, with some modest reductions in hiring compared to typical years. This reflects the challenges these industries have faced during the pandemic, namely with respect to increased difficulty with sales, hiring and, somewhat surprisingly, inefficiencies from remote work. Aerospace has not yet recovered from the initial impacts of the pandemic, still reeling from significant hits to both sales and employment, as well as disruptions in their supply chains from lockdowns and restricted international travel and transportation.

Smaller firms are looking to add space

After more than a year of implementing remote work and reduced onsite staffing, companies are beginning to plan for a return to the office. However, how much space awaits those returning to the office will vary by industry as well as firm size.

It is small- and medium-sized firms that are looking to expand their commercial real estate footprint over the next year rather than larger firms. In fact, the proportion of firms surveyed that expect to increase space by 10 percent or more of their current square footage is nearly double that of those planning to reduce their current space by 10 percent or more (16 percent to 8.4 percent, respectively). However, when you factor in the size of each company, those planning significant real estate growth represent only three percent of the jobs compared to 13 percent of jobs for those looking to reduce space significantly (companies surveyed collectively employ nearly 200,000 workers).

When we look at the innovation companies, we see some stark differences between traditional Technology and Biotechnology industries. Eight percent of respondents representing 22 percent of jobs plan to reduce their space by more than 10 percent—mostly in the Telecommunications industry. However, nearly 26 percent of respondents representing 41 percent jobs expect to add modest amounts of space less than 10 percent of their current footprint. Here many respondents are in the Biomedical Device and Biotech industries and likely in need of additional production or lab space.

Understanding these evolving and distinct trends is important because San Diego’s innovation cluster is leading the region out of this pandemic-driven economic downturn, just as it has in each past downturn. Each job added in the innovation cluster supports another two jobs elsewhere in the economy. Yet, these innovation companies do not necessarily need to be physically located in San Diego in order to operate. Making sure these companies have the infrastructure and access to talent that they need to flourish is critical to our region’s prosperity.

Stay tuned for more on San Diego’s changing business landscape. EDC will be back every other month with more trends and insights. For more data and analysis visit: sandiegobusiness.org/research.

Each month the California Employment Development Department (EDD) releases employment data for the prior month. This edition of San Diego’s Data Bites (formerly the Economic Pulse) covers March 2021 and reflects the lingering effects of the coronavirus pandemic on the region’s labor market. Check out EDC’s Research Bureau for more data and stats about San Diego’s economy.

Key Takeaways

San Diego establishments added 9,900 new payroll positions in March, but gains were uneven across industries.

The unemployment rate edged lower to 6.9 percent from February’s 7.2 percent. However, this was due primarily to the loss of 10,300 workers from the labor force.

Consumer spending has improved significantly as households spend stimulus checks and unwind the savings accrued over the past year or so; this could mean tens of thousands of jobs in Leisure and Hospitality and Retail in the coming two to three months.

First glance

The March jobs report for San Diego was a mixed bag. Employers added 9,900 new payroll positions, and the unemployment rate edged lower to 6.9 percent from 7.2 percent in February. However, job growth was uneven across industries, with gains in Leisure and Hospitality, Professional and Business Services, and Government partially offset by declines in Construction, Manufacturing, and Retail. Moreover, 10,300 workers left the job market in March—or roughly a third of the 29,800 people who either joined or rejoined the labor force in February. In fact, it was the loss of these workers that pushed the unemployment rate lower more than employment gains.

Industry view

Job gains were apparent in just nine of the 16 supersectors tracked by the EDD. This is somewhat surprising, given March’s blowout employment report for the U.S., which showed nearly a million new jobs were created.

Leisure and Hospitality establishments added 5,000 jobs in March, building on the 13,200 positions recovered in February. Also encouraging, more than half of these jobs came from restaurants. Meanwhile, Professional and Business Services logged an additional 3,300 positions thanks to a big push from the crucial Professional, Scientific, and Technical Services segment, which notched 2,900 more jobs in March than the month prior.

Builders let go of 1,500 workers in March, reversing most of the 2,100-worker gain from February. And, while losses in Construction aren’t completely unheard of in March, they’re certainly the exception rather than the rule. Builders have let go of workers in March in only seven of the past 31 years.

Manufacturing, Retail, Finance, and Real Estate companies let go of a combined 1,100 workers in March. These figures may reflect some statistical noise and potentially even some buyback after February’s strong report. Nonetheless, the loss of 400 Retail positions is a surprise, especially following the March U.S. retail sales report, which showed a huge rebound in consumer spending last month.

Relief for Hospitality and Retail is (finally) on the way

U.S. retail sales, which include sales at restaurants and bars, jumped by 9.8 percent in March, blowing past analysts’ expectations. The meteoric rise was in large part the result of stimulus payments that were distributed to millions of households last month as part of the Biden administration’s $1.9 trillion COVID-19 rescue package.

In addition to stimulus-related spending, consumers may have also begun unwinding some of their savings now that a sustained recovery appears to be in the offing. To be sure, households began hoarding cash at the onset of the downturn last year. The U.S. personal saving rate peaked at 33.7 percent last April, decimating the previous record of 17.3 percent that was set in May 1975, and remained perched at an elevated 13.6 percent in February 2021, which is nearly double the pre-pandemic average of 7.3 percent observed between 2010 and the end of 2019.

As long as the news around COVID cases continues to be positive and residents continue to be vaccinated at current rates, it’s not unreasonable to suspect that consumers will continue to spend freely into the summer and fall months.

This is particularly good news for San Diego’s restaurant and bar scene. Given the region’s status as a premier tourist destination, changes in national spending at eating and drinking establishments correlate strongly with job growth here at home. If sustained, March’s leap in U.S. retail sales could mean as many as 50,000 to 60,000 payroll positions at San Diego’s bars and restaurants, in addition to March’s jobs build as employers continue to meet rising demand.

Retailers can also expect a big boost. If historical relationships hold, 15,000 to 20,000 positions could appear in April and May if consumers continue to loosen their purse strings. The correlation between local Retail employment and national consumer spending is quite a bit looser than the relationship for eating and drinking places. However, as a point of comparison, local consumer spending data from Affinity also reveal a rebound, which reinforces the notion that job gains will continue for at least the next several months barring any unexpected hiccups.

Bottom line

Even though it wasn’t quite as strong as expected, March’s employment report is further evidence that the job market has finally turned the corner after a temporary slump in December and January. Nonetheless, it will still take some time before the damage wrought by the COVID downturn is undone. Payroll employment is still 7.2 percent below year-ago levels and 8.1 percent lower than the pre-pandemic level reached in February 2020. Moreover, the unemployment rate remains elevated, and 57,140 workers are still missing from the labor force.

It will also be imperative that San Diego small businesses are connected to large buyers in order to keep remaining businesses in the region healthy and to help spur a new wave of entrepreneurship to meet the needs of San Diego’s largest institutions and employers. EDC’s Anchor Collaborative is working with large local businesses to help ensure big companies “shop local” for their procurement needs. Our research estimates that a one percent shift in procurement spending by large companies to local businesses could create thousands of new jobs in the region.

EDC is excited to unveil a fresh take on our long-standing Economic Pulse. Welcome to San Diego’s Data Bites!

Each month the California Employment Development Department (EDD) releases employment data for the prior month. This edition of San Diego’s Economic Pulse—now ‘Data Bites’—covers January 2021 and reflects the effects of the coronavirus pandemic on the labor market as well as benchmark revisions to 2020 employment data. Check out EDC’s Research Bureau for more data and stats about San Diego’s economy.

Key Takeaways

San Diego employers eliminated 38,600 payroll jobs at the start of the year. Job losses in January are typical as temporary holiday staff is let go, but December’s report showed no surge in holiday hiring in 2020.

Job losses nudged the unemployment rate higher to 8.1 percent from December’s 8.0 percent even as nearly 18,000 workers fled the labor force.

Annual benchmark revisions to 2020 employment data revealed that the economy suffered steeper job losses last Spring and ended 2020 with roughly 30,000 fewer jobs than were initially reported.

San Diego’s labor market kicked off 2021 on a sour note. Local employers eliminated 38,600 payroll jobs in January, nudging the unemployment rate higher to 8.1 percent from 8.0 percent in December even as nearly 18,000 workers fled the labor force.

Job losses are typical in January as businesses roll off temporary holiday help. However, what makes this report unique is that January’s job losses followed a decline of 6,200 positions in December (revised from an initially reported -5,300 jobs), which is extremely atypical for the holiday season. In fact, December’s decline marks only the sixth time in 72 years where employers have let more workers go than they hired.

January’s dismal jobs report likely reflects the struggles of local businesses amid the ongoing COVID-19 pandemic rather than seasonal factors. Burning Glass estimates that San Diego consumer spending is still trending about 10 percent lower than it was before the pandemic, and data from Womply show that roughly 30 percent to 40 percent—or between 30,000 and 40,000—local businesses have been forced to close over the past year.

Industry view

Employment declines were widespread across industries. With the exception of Manufacturing and Utilities—which added a meager 100 jobs apiece—every industry either lost jobs or stayed flat. Hardest hit was Leisure and Hospitality, which gave up 12,200 positions and continues to be the most negatively impacted by the pandemic. Retail, which shed 6,300 jobs, was a distant second, erasing nearly all of the gains made since Spring 2020. The decline in Retail, although disheartening, was somewhat expected, however, since national retail sales and local consumer spending have both remained weak in recent months.

The nearly ubiquitous loss of employment across industries is another indication that labor market weakness in January stems from COVID-related measures rather than seasonality. In a typical year, January job losses would be focused around Leisure, Hospitality, and Retail as holiday staff is let go. However, in more normal times, most other industries have remained stable instead of laying off workers like they did this year.

2020 was even worse than we thought

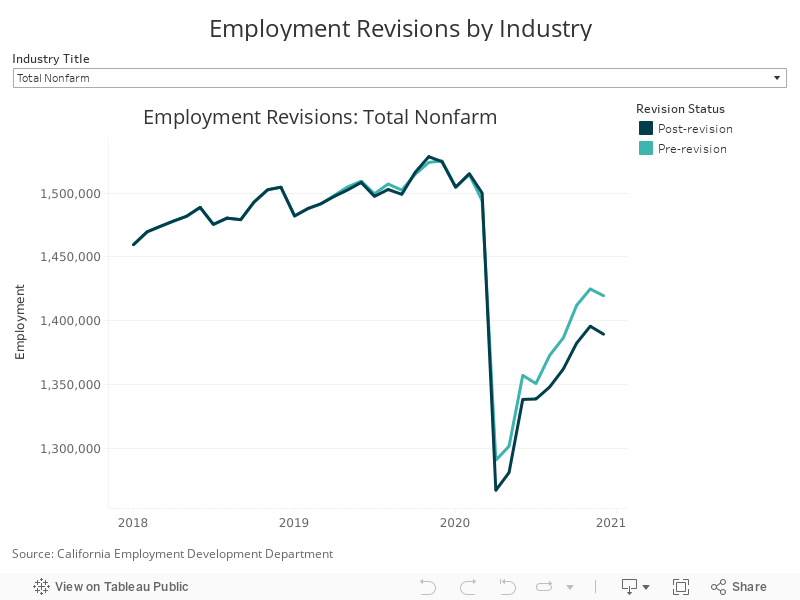

Also included in January’s jobs report were benchmark revisions to the 2020 employment figures. Typically, in periods of contraction, employment revisions are negative, and that is exactly what EDD reported.

Benchmark revisions revealed that San Diego hemorrhaged 248,000 jobs between February and April 2020, which is 25,000 more job losses than initially reported. Leisure, Hospitality, and Retail accounted for around 16,000 of those additional losses. By the end of the year, revisions showed 30,100 fewer nonfarm payroll jobs in the region compared to the initial estimates.

The additional loss of jobs also meant that the unemployment rate was revised higher. Initial estimates showed the rate peaking at 15.2 percent in April 2020; revised data revealed that joblessness peaked at a significantly higher 15.9 percent, which is more in line with EDC’s estimates at the time.

You can use the below graphic to explore how revisions impacted total employment in the region, as well as each of the industries tracked by EDD on a monthly basis.

The road ahead

San Diego’s job market is entering 2021 on a weaker footing than initially thought. More jobs need to be recouped, and there are fewer businesses to help carry that weight. Together, this implies that the recovery will take longer than anticipated even after San Diegans have been vaccinated against the novel Coronavirus.

Training and upskilling will be vital for the thousands of workers whose jobs may never return. EDC’s Advancing San Diego program is working to do just that.

It will also be imperative that San Diego small businesses are connected to large buyers in order to keep remaining businesses in the region healthy and to help spur a new wave of entrepreneurship to meet the needs of San Diego’s largest institutions and employers. EDC’s Anchor Collaborative is working with large local businesses to help ensure big companies “shop local” for their procurement needs. Our research estimates that a one percent shift in procurement spending by large companies to local businesses could create thousands of new jobs in the region.